AI voice agents can legally negotiate payment plans during debt-collection calls when built on compliance-first architectures. Real-time FDCPA monitoring, mandatory human escalation, and integrated payment processors define the platforms leading this category.

Key Takeaways

AI payment-plan negotiation is FDCPA-compliant when platforms enforce call-time restrictions, deliver Mini-Miranda disclosures, and escalate disputes to human agents in real time.

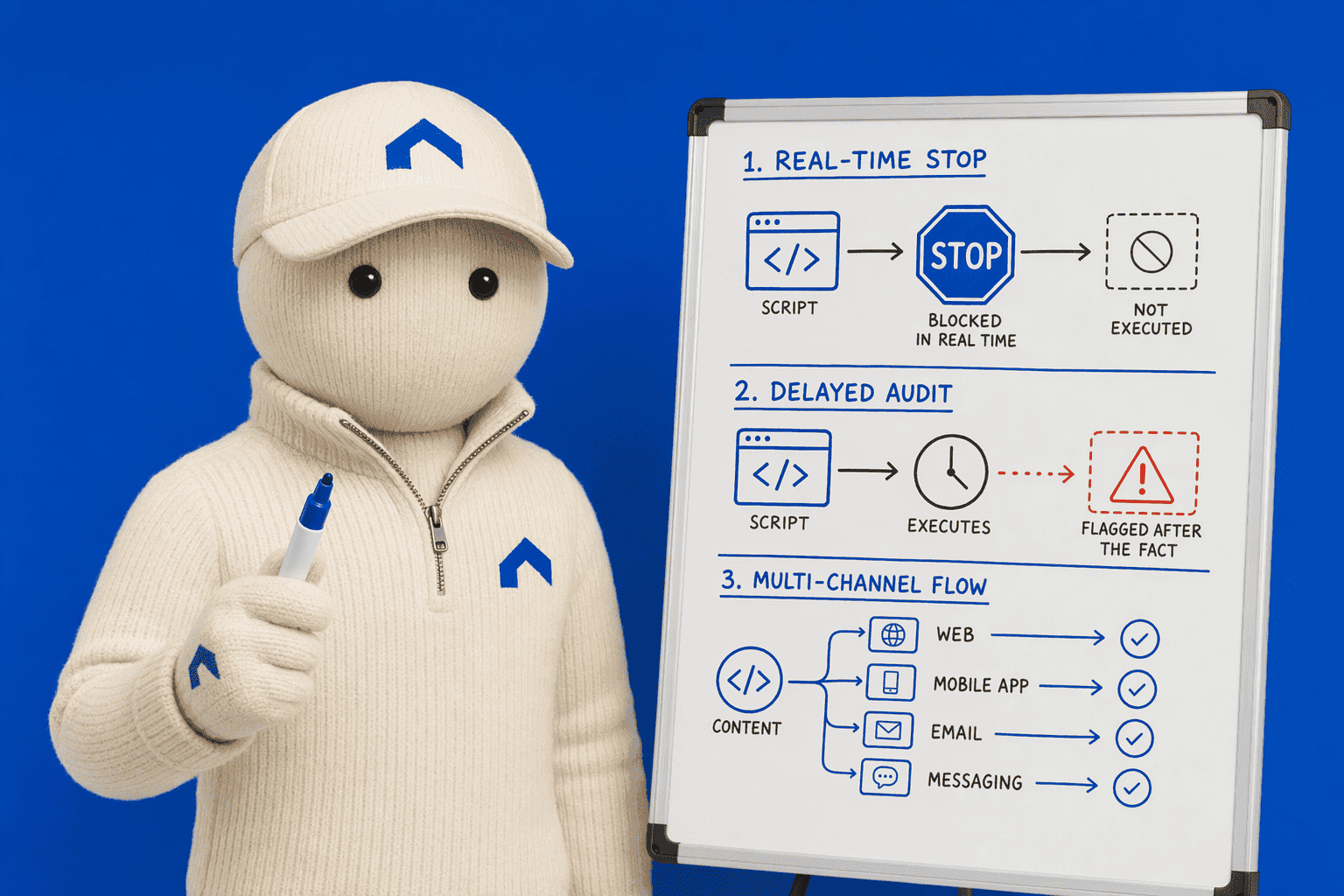

Real-time compliance monitoring platforms intercept live transcripts and halt scripts before violations reach debtors, whereas post-call audits catch violations too late.

Omnichannel orchestrators coordinate voice, SMS, and email around payment-plan attempts using behavioral signals to optimize timing and channel choice.

Emotion-detection layers analyze stress and sentiment to trigger human escalation when distress thresholds exceed safe negotiation boundaries.

Portfolio complexity—dispute rates, validation requests, and channel requirements—determines whether rigid-script, dynamic-adaptation, or omnichannel platforms deliver optimal ROI.

What Makes AI Payment-Plan Negotiation Fdcpa-Compliant?

Yes—AI can negotiate payment plans during phone calls, but compliance safety depends entirely on the platform's architectural foundation. Platforms like Vodex, Retell AI, Domu, and Floatbot automate voice conversations for debt collection while maintaining FDCPA, TCPA, and Regulation F compliance through built-in regulatory engines, automated disclosure delivery, and consent documentation. The difference between a compliant system and a regulatory liability comes down to three core architectural layers: real-time compliance monitoring, omnichannel orchestration, and emotion-detection guardrails.

The Compliance Question: Can AI Negotiate Without Triggering Violations?

The FDCPA prohibits debt collectors from placing repeated or continuous telephone calls to annoy, abuse, or harass debtors, and sets strict boundaries: calls must occur between 8 a.m. And 9 p.m. Local time, and collectors are presumed to violate the law after more than seven calls within a seven-day period. Regulation F further prohibits false or misleading representations and unfair practices in debt collection. AI platforms must enforce these rules automatically—call-time windows, frequency caps, Mini-Miranda disclosures, and cease-and-desist handling, without requiring manual oversight on every interaction.

Three Architectural Approaches to Safe Negotiation

Real-time compliance monitoring platforms detect inappropriate legal language and threats during live calls, halting scripts before violations reach debtors. Domu's Alex module stress-tests conversation flows against FDCPA and TCPA boundaries in a synthetic environment before deployment, while Jordan validates customer interactions against UDAAP and state-specific collection laws after deployment. Omnichannel orchestration systems unify voice, SMS, and email workflows to prevent frequency violations across channels. Emotion-detection layers identify debtor distress signals and trigger human escalation before conversations escalate into harassment claims.

The Trade-Off: Rigid Scripts Vs. Dynamic Adaptation

Platforms that adapt payment offers mid-call based on debtor responses require stronger compliance guardrails than those following fixed scripts. Dynamic negotiation engines must validate every offer variation against FDCPA misrepresentation rules in real time, while script-based systems can pre-certify all possible conversation paths. At Domu, we believe adaptive AI requires pre-deployment stress-testing and post-deployment monitoring to maintain compliance without sacrificing conversational flexibility, a balance that distinguishes governance-first platforms from general-purpose voice bots.

Understanding the compliance foundation is the first step; next, examine how platforms enforce those rules during live conversations.

Real-Time Compliance Monitoring Platforms

How Real-Time Intervention Works During Payment-Plan Calls

Real-time compliance monitoring platforms enforce FDCPA, TCPA, and Regulation F boundaries by intercepting live conversation transcripts, evaluating each utterance against a policy engine, and correcting or escalating violations before they reach the customer. The workflow unfolds in four steps:

Transcript capture, voice-to-text engines convert the agent's speech into text with sub-second latency.

Policy engine evaluation, the transcript fragment is matched against a rule set covering prohibited language, disclosure timing, Mini-Miranda delivery, and call-window restrictions.

Agent correction or flag, when a violation is detected, the system either blocks the utterance before transmission, prompts the agent with compliant phrasing, or flags the call for immediate review.

Human escalation, calls that trigger mandatory escalation triggers (disputes, validation requests, cease-and-desist) are routed to a live supervisor within seconds.

Autocalls.ai offers FDCPA-aware features such as Mini-Miranda delivery, call-time restrictions, and cease-and-desist handling within a general voice platform, though it is not a purpose-built compliance architecture. Retell AI provides voice-agent infrastructure with integrations to debt-collection and payment platforms, reducing operational costs by approximately 90% according to vendor claims, though vendor-reported savings are not standardized benchmarks and actual ROI depends on deployment model, case complexity, and baseline staffing costs.

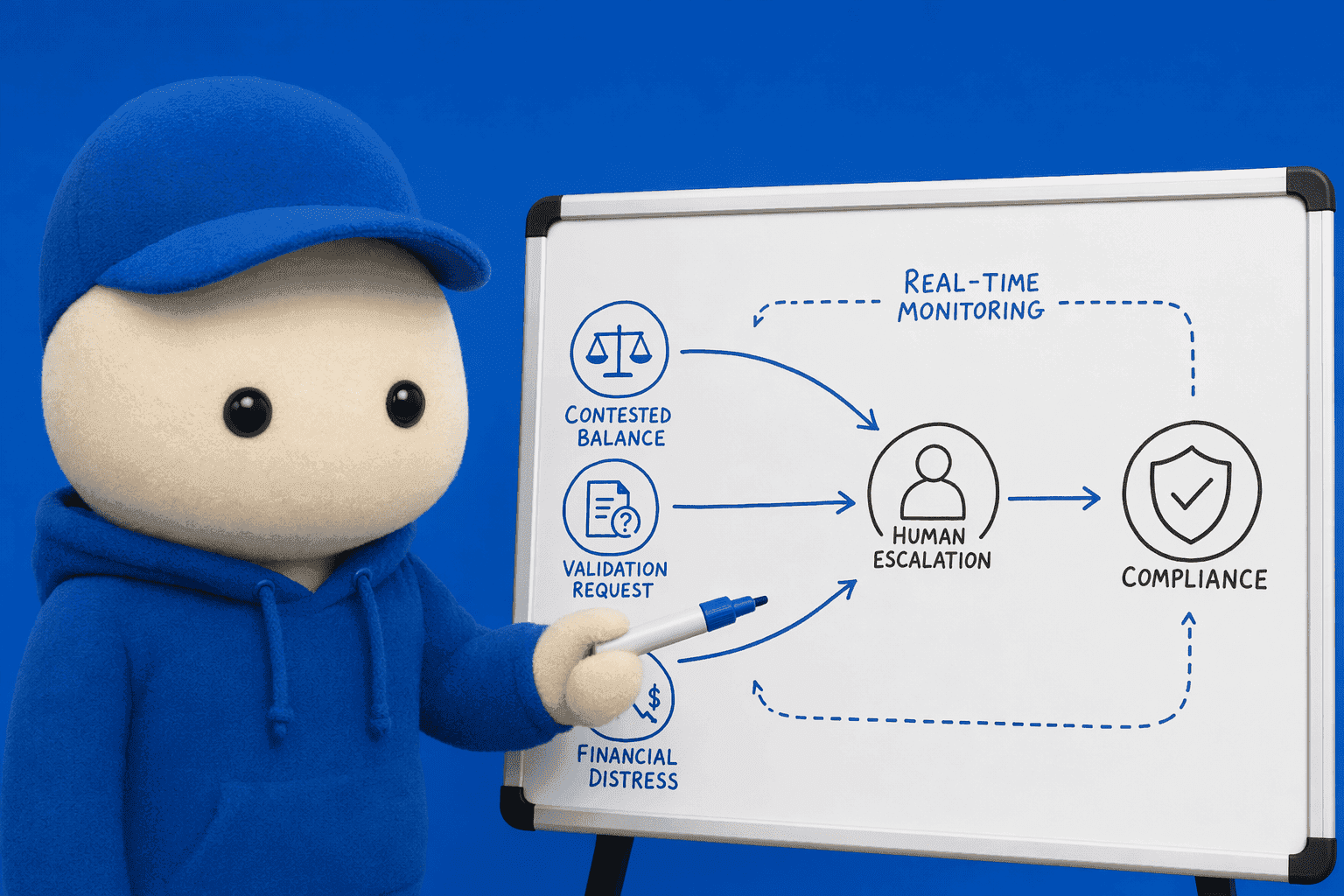

Mandatory Human Escalation Triggers

FDCPA rules require human intervention when AI detects disputes, validation requests, high-stress sentiment indicators, or cease-and-desist language. These triggers cannot be resolved by automated agents because they demand judgment, documentation, and immediate cessation of collection activity. Platforms that route these scenarios to a live supervisor in real time protect institutions from regulatory exposure while preserving the customer relationship.

Integration Requirements: CRM, Payment Processors, and Dialers

Deploying a real-time monitoring agent presupposes integration with existing CRM systems (to pull account history and dispute flags), payment processors (to confirm transaction status and plan eligibility), and dialers (to manage call routing and recording). Without these connections, the compliance engine cannot access the context needed to evaluate whether a statement is permissible or which escalation path to trigger.

Real-time monitoring solves one piece of the compliance puzzle. For multi-touch campaigns, orchestration platforms extend enforcement across voice, SMS, and email.

Omnichannel Orchestration + Behavioral Intelligence

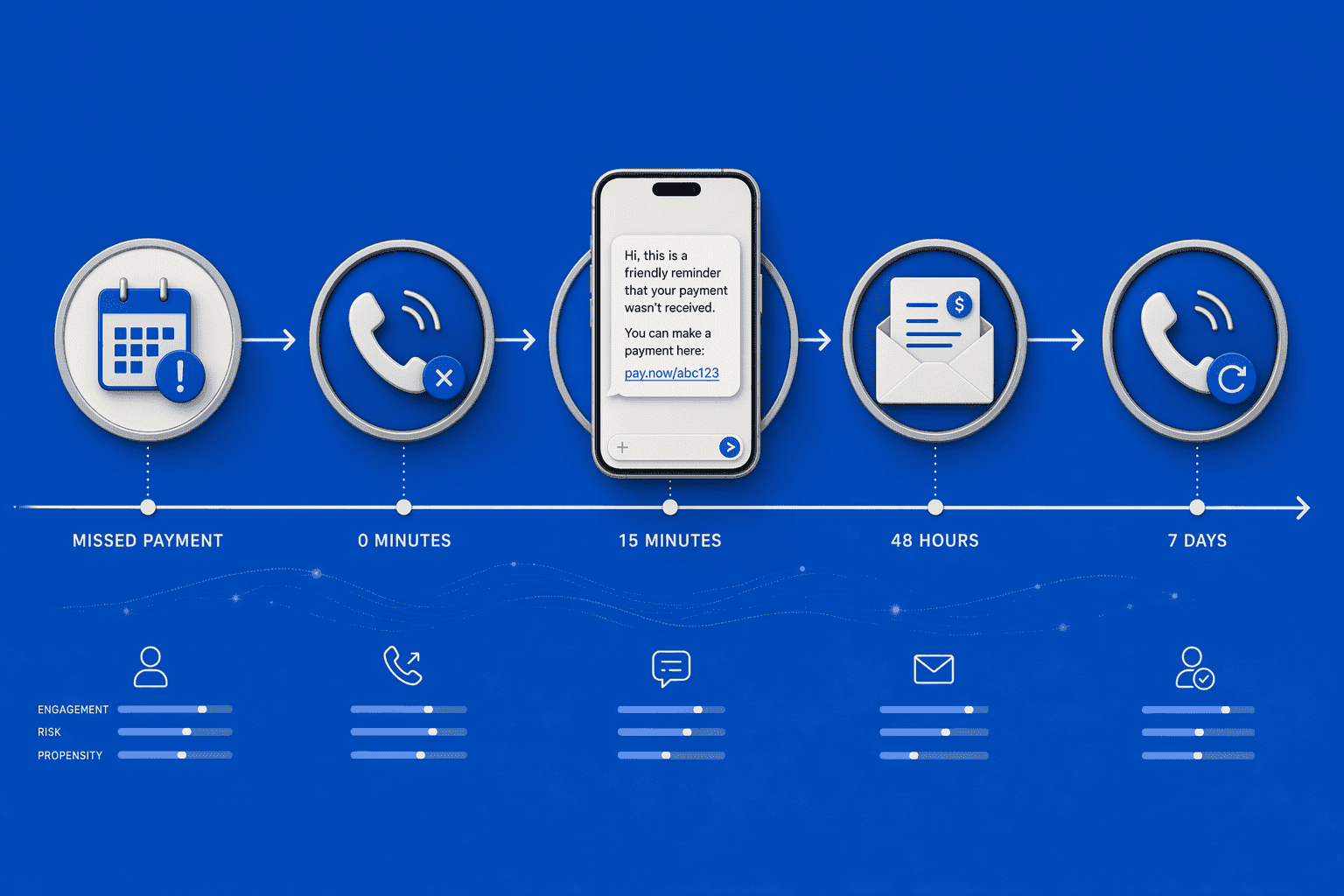

Platforms that coordinate voice, SMS, and email sequences around payment-plan attempts use behavioral signals to optimize negotiation timing and channel choice. Domu unifies Voice, Email, and SMS across the customer lifecycle, with behavioral signals feeding decisions in real time rather than after the fact. The orchestration workflow typically follows this sequence: Debtor misses a payment → voice call attempt fails → SMS with payment link sent within 2 hours → email follow-up at 48 hours if no SMS response → voice re-attempt at 7 days if no payment. This channel cascade ensures debtors receive outreach through their preferred contact mode without violating frequency caps.

How Omnichannel Orchestration Coordinates After Failed Call Attempts

When a voice negotiation attempt fails, the system triggers immediate SMS follow-up with a payment link, then email if no response within 48 hours. Domu's AI agents handle calls, texts, and emails as one coordinated campaign rather than three disconnected channels. The CollectDebt.ai platform focuses on predictive segmentation ahead of campaigns rather than real-time call adaptation, it optimizes campaign targeting before outreach begins, whereas Domu adjusts channel strategy mid-sequence based on live debtor behavior. This distinction separates pre-campaign optimization from in-flight orchestration.

Behavioral Intelligence: Adjusting Offers Based on Debtor Responses

Platforms analyze response signals, open rates, click-through, partial payments, to adjust next offers without violating FDCPA script rules. Domu's behavioral intelligence capabilities link payment pattern cohorts to pre-approved message templates that vary tone, urgency, and call-to-action based on debtor profiles. The trade-off: platforms that adjust payment offers based on debtor responses must stay within FDCPA script boundaries. Rigid offer structures carry lower violation risk but reduced success rates; adaptive offers improve recovery but require stronger guardrails to prevent off-script escalation.

Digital-First Vs. Voice-First Trade-Offs

Some platforms lead with email and SMS, reserving voice calls for escalation when digital channels fail. Others start with voice attempts, then fall back to digital. Voice-first approaches deliver higher right-party contact rates but consume more agent capacity; digital-first strategies scale efficiently but often yield lower immediate engagement. ClaraPay exemplifies the AI-powered orchestration category, balancing automated voice agents with conversational SMS for text-based outreach. The optimal sequence depends on debtor segment: high-balance accounts benefit from voice-first contact, while low-balance portfolios justify digital-first efficiency.

Teams with existing dialer infrastructure often prefer bolt-on intelligence layers over full voice replacements. Emotion-detection modules fit that use case.

Emotion-Detection Layers Without Native Voice

How Emotion Detection Works as a Partner-Distributed Module

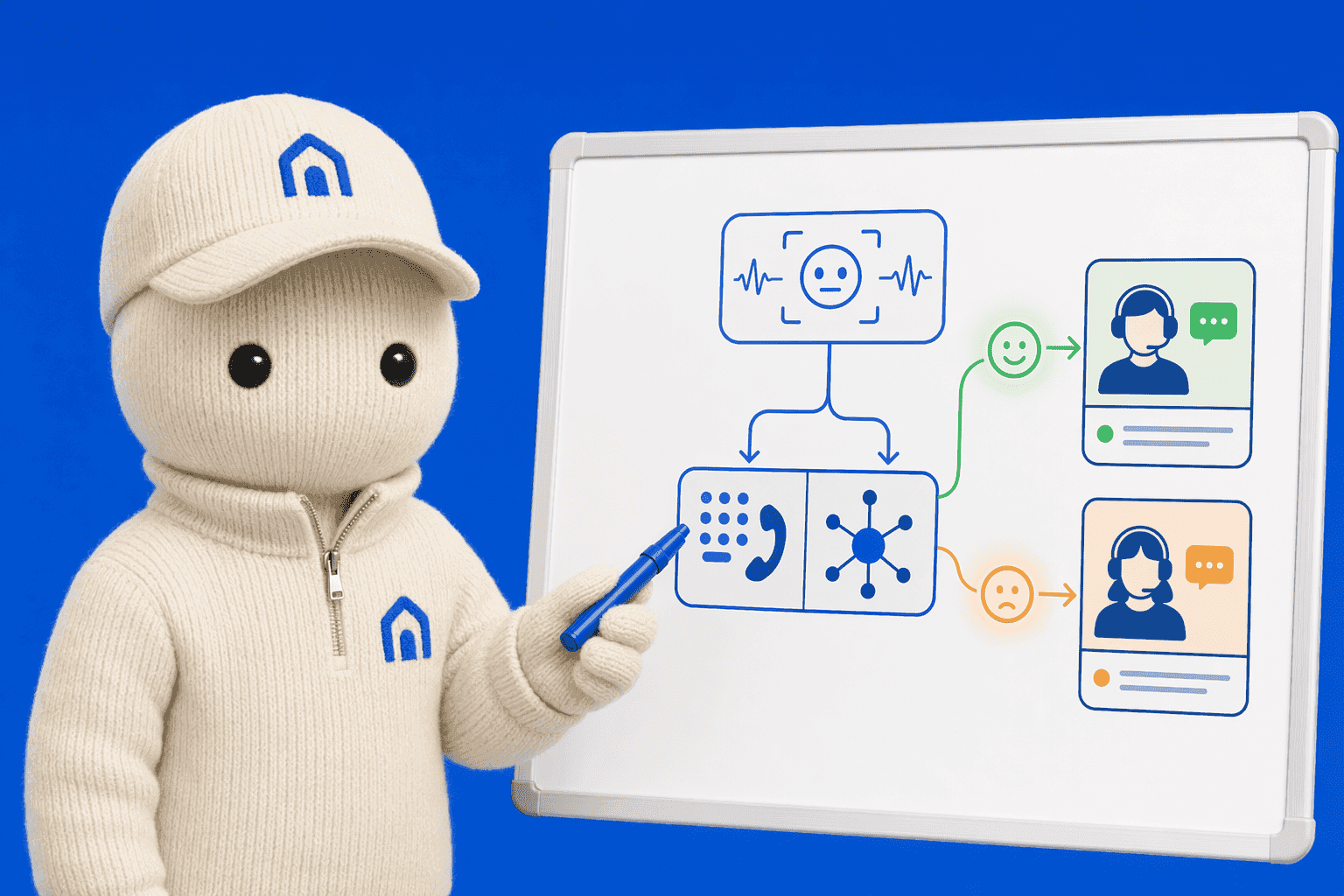

Emotion-detection layers analyze stress, sentiment, and conversational cues during calls but do not handle the voice infrastructure themselves. These modules integrate with existing dialers or routing platforms, providing stress scores and sentiment flags that inform real-time decision-making. Unlike end-to-end voice platforms that unify calling, script enforcement, and emotion analysis in one system, emotion-detection layers operate as partner-distributed modules, feeding behavioral intelligence into separate collections or customer-service platforms. This architecture suits teams that already operate call centers and want to layer behavioral insight onto their existing infrastructure without replacing their core dialer technology.

Use Cases: Escalation Triggers and Agent Coaching

Stress scoring translates into actionable escalation decisions: when a debtor's stress metric exceeds a defined threshold (for example, 7 out of 10), the system routes the call to a human agent trained in de-escalation. Post-call, the same sentiment data informs agent coaching, supervisors review flagged interactions to identify where tone or pacing could improve. AI-powered predictive analytics in debt collection demonstrate how behavioral data drives both real-time routing and retrospective training workflows, improving repayment rates while reducing complaint volume.

When to Choose Emotion Detection Vs. Integrated Voice Platforms

The decision hinges on deployment model: emotion-detection layers suit teams with mature dialer infrastructure who want to add behavioral intelligence without rebuilding their call stack. Integrated voice platforms, which combine calling, script enforcement, compliance controls, and sentiment analysis, suit teams building from scratch or replacing legacy systems. Platforms like GetBill illustrate the integrated approach, handling the entire collections workflow by phone. Emotion detection alone does not prove collections readiness; it must pair with compliance enforcement to meet FDCPA requirements.

With architectural categories defined, direct comparison reveals how platforms differ on compliance enforcement, channel breadth, and negotiation flexibility.

Comparison: Compliance Architecture, Channel Support, and Negotiation Flexibility

Table: Platform Comparison Matrix

Platform | Compliance Enforcement | Channel Support | Negotiation Flexibility | Best For |

|---|---|---|---|---|

Domu | Real-time policy flagging with governance certification and human escalation paths | Voice, SMS, Email unified across lifecycle | Adaptive payment plans within compliance template library | Regulated portfolios requiring real-time compliance enforcement and omnichannel orchestration |

Retell AI | Developer-configured compliance rules | Voice-only; requires separate SMS/email integration | Custom negotiation logic via API | Teams with technical resources to build custom integrations |

AutoCalls.ai | Post-call audit with Mini-Miranda delivery | Voice-first; basic SMS support | Rule-based offer structure | General voice campaigns with basic FDCPA awareness |

AgentApex | Configurable compliance checks | Voice and SMS | Template-driven negotiation flows | Mid-market agencies seeking voice automation with moderate compliance needs |

Smallest.ai | Script-based compliance guardrails | Voice-only | Fixed payment-plan options | Small-scale operations prioritizing simplicity over flexibility |

Reading the Comparison: Real-Time Intervention Vs. Post-Call Audit

The compliance-architecture column distinguishes platforms that enforce regulatory boundaries *during* the conversation from those that audit *after*. Real-time intervention, such as Domu's governance certification workflow, detects inappropriate legal language and halts scripts before violations reach consumers. Post-call audit models flag issues only in review, creating exposure windows where non-compliant statements already occurred. For portfolios with high dispute rates or complex hardship scenarios, real-time enforcement mitigates regulatory risk at the point of contact rather than retrospectively.

Channel Support and Integration Complexity

Voice-only platforms require separate tools for SMS and email, fragmenting consent management and interaction history. Omnichannel systems like Domu coordinate calls, texts, and emails as one campaign, synchronizing consent across channels and maintaining continuity when a consumer switches from voice to text mid-conversation. Integration complexity scales with channel count: unified platforms demand CRM, payment processor, and dialer connections but eliminate manual handoffs between channel-specific vendors.

Ready to see your future AI agents in action? Compare platforms side-by-side to find the compliance and channel architecture that fits your servicing workflow.

The comparison table highlights structural differences; now translate those distinctions into portfolio-specific deployment decisions.

Which Platform Fits Your Debt Portfolio?

High-Dispute Portfolios: Real-Time Compliance Monitoring Required

Portfolios with frequent validation requests, contested balances, or customers showing signs of financial distress demand platforms that escalate to humans mid-call when the AI detects elevated dispute likelihood. Under FDCPA rules, disputes and validation requests trigger mandatory procedural steps that AI cannot complete alone. Regulatory compliance frameworks emphasize that high-stress sentiment and contested claims remain human-escalation scenarios. Domu, for example, enforces compliance as a constraint built into the architecture, with real-time policy flagging and human escalation paths.

Straightforward Repayment Scheduling: Rigid Scripts Sufficient

Simple payment-plan workflows, fixed installment offers with no counter-negotiation, can rely on rigid-script platforms with lower compliance overhead. When accounts carry minimal dispute history and borrowers typically accept standard terms, the AI operates within narrow guardrails and requires less dynamic adaptation. This approach reduces the need for sophisticated behavioral intelligence layers while maintaining on-script enforcement.

Omnichannel Campaigns: Behavioral Intelligence + Voice Coordination

AI-driven collections platforms running multi-touch campaigns across voice, SMS, and email need behavioral intelligence that tracks context across channels. Omnichannel orchestration ensures each touchpoint aligns with compliance mandates and prior interaction history, preventing duplicate outreach and conflicting promises. Ready to see your future AI agents in action? Review platform comparisons that map architecture to portfolio needs.

Conclusion

Rigid-script platforms minimize violation risk but limit negotiation flexibility, dynamic adaptation platforms achieve higher success rates but require real-time compliance guardrails and audit trails. Voice-first platforms suit portfolios where phone contact is the primary channel; omnichannel orchestrators suit teams running multi-touch campaigns across voice, SMS, and email with behavioral intelligence. As AI voice agents mature, regulatory scrutiny will intensify around consent, transparency, and audit trails, platforms that embed compliance as architecture rather than add-on features will lead the next generation of payment-plan negotiation. Evaluate your portfolio's dispute rate and channel mix, then explore Domu's real-time compliance monitoring and omnichannel orchestration to deploy FDCPA-safe payment-plan negotiation at scale.

Frequently Asked Questions

Can AI legally negotiate payment plans during debt-collection phone calls?

Yes, when platforms enforce FDCPA rules in real time, Mini-Miranda delivery, call-time restrictions, and human escalation for disputes. Domu builds compliance as an architectural constraint with real-time policy flagging and mandatory escalation paths.

What is the difference between real-time compliance monitoring and post-call audit?

Real-time monitoring analyzes transcripts during the call and intervenes, correcting the agent or escalating to a human, when policy violations are detected. Post-call audit reviews recordings after the fact, catching violations too late to prevent FDCPA exposure.

How do AI platforms handle cease-and-desist requests during calls?

Platforms detect cease-and-desist language in real time, immediately stop collection attempts, flag the account, and route future contacts through legal review. Autocalls.ai includes cease-and-desist handling as a baseline compliance feature.

What pricing models do AI payment-plan negotiation platforms use?

Three common models: per-call (fixed fee per completed call), per-minute (usage-based, suits high-volume campaigns), and agent-based licensing (monthly seat fee, suits teams replacing human agents). High-volume portfolios favor per-minute; low-volume portfolios favor per-call models.

When must AI negotiation agents escalate to human collectors?

Mandatory escalation triggers include disputes about the debt, validation requests, high-stress sentiment (stress score >7/10), cease-and-desist requests, and subjective hardship cases. These thresholds protect FDCPA compliance and preserve debtor relationships during sensitive negotiations.

Do AI debt-collection agents actually reduce headcount or just shift workload?

Depends on deployment model and case complexity. Vendor-reported savings are not standardized benchmarks; actual ROI depends on deployment model, case complexity, and baseline staffing costs. Simple payment plans reduce headcount; high-dispute portfolios shift workload to oversight roles.

What systems must be in place before deploying an AI payment-plan negotiation agent?

Prerequisites include CRM (to store debtor records), payment processor (to execute payment plans), and dialer (to handle call routing). Typical API integration timelines run 4-8 weeks. Without these connections, compliance monitoring and payment-plan execution fail.

Sources

When and how often can a debt collector call me on the phone? - consumerfinance.gov (2024)

Debt Collection Practices (Regulation F): Final rule - files.consumerfinance.gov (2020)

Frequently Asked Questions - startupfinanceguide.com (2026)

AI for Debt Collection — Voice AI Agents for Payment Recovery - autocalls.ai

Powerful AI Phone Agent for Debt Collection - Retell AI - www.retellai.com

10 minutes

Explore Related Articles

GET STARTED

We’re building the next generation of engagement technology: intelligent, automated, and compliant. Our mission is to empower financial institutions to orchestrate every stage of the servicing lifecycle with dignity and unprecedented efficiency.

Supported by

Y Combinator

AWS

Microsoft