Traditional debt collection operations consume 30-80% of recovery amounts in overhead, yet automation introduces regulatory risk. Behavioral intelligence platforms promise to cut costs while preserving compliant, empathetic customer interactions.

Key Takeaways

Evaluate platforms across compliance architecture, behavioral analytics depth, integration capabilities, and conversation quality as sequential filters.

Pre-deployment governance—stress-testing conversation flows with synthetic scenarios—prevents violations before customer contact, while post-deployment monitoring only flags issues in production.

Agent-based voice bots excel at high-volume standardized collections; orchestration platforms cut cost-per-contact through omnichannel routing; hybrid models pair AI-first engagement with human escalation for complex disputes.

Audit-ready evidence includes conversation transcripts, decision logs, compliance rule triggers, and explainability artifacts that risk committees and regulators can review.

Recovery rate lift claims range from 42% to 72%, but actual ROI depends on deployment model, case complexity, and baseline performance.

What Financial Institutions Need in Behavioral Intelligence Platforms

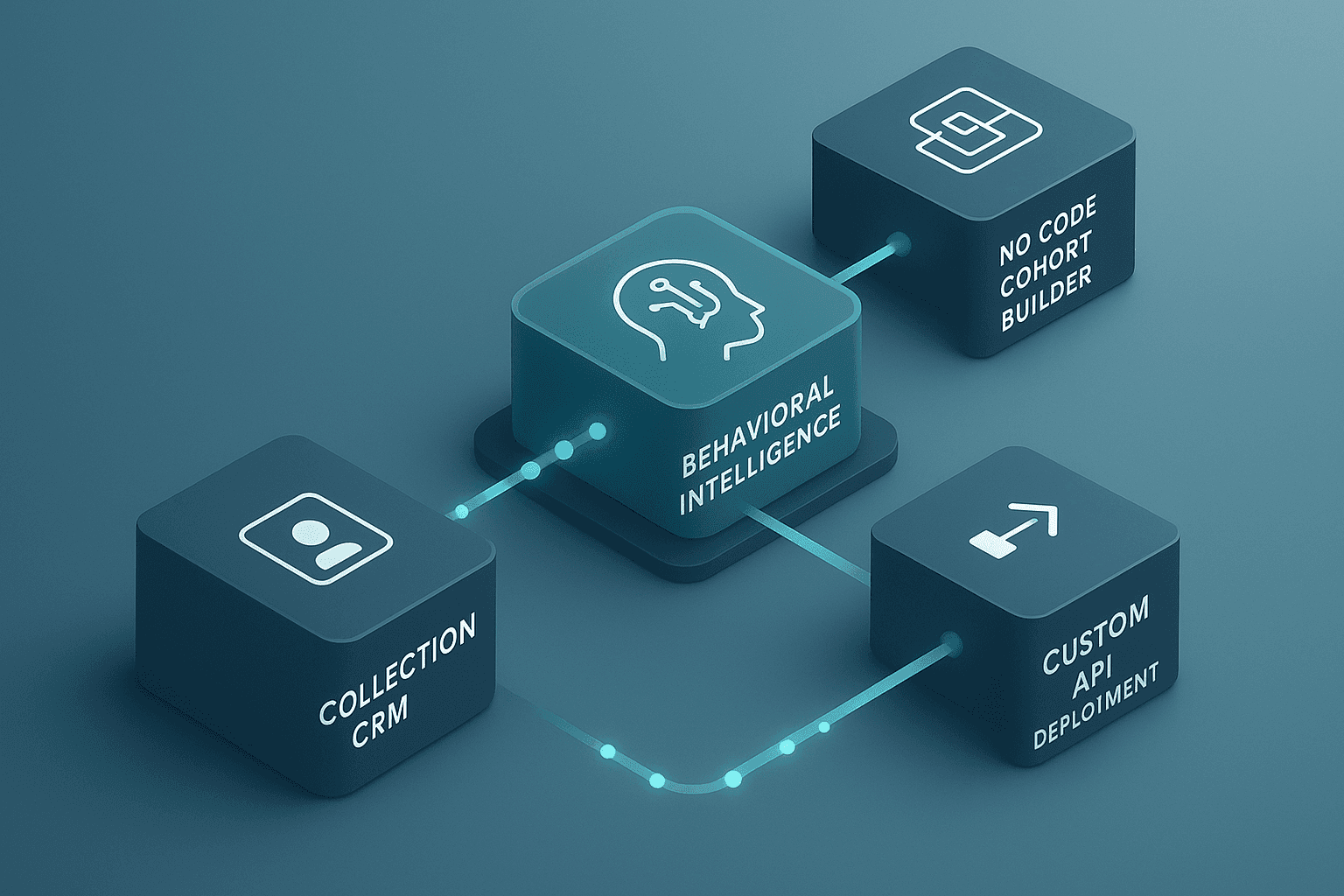

AI voice bots, conversational orchestration platforms, and omnichannel messaging systems form the three core tool categories that help reduce collection costs while maintaining human-like customer conversations. Each automates different stages of the engagement lifecycle — from initial contact to payment negotiation — but selecting the right platform requires evaluating four critical dimensions that separate compliance-ready systems from operational liabilities.

The Core Challenge: Cost Reduction Without Compliance Risk

Financial institutions face a stark tension: traditional collection operations consume 30-80% of recovery amounts in operational overhead, yet automation introduces regulatory exposure under FDCPA and TCPA guidelines [1]. The baseline reality — agencies recover between $20 and $30 for every $100 in outstanding debt[2], means efficiency gains directly impact net recovery. Platforms that promise cost reduction without embedded compliance architecture shift risk from vendor to institution, a trade-off few compliance officers will accept after Reg F enforcement actions demonstrated the liability of inadequate guardrails.

Four Evaluation Pillars for Platform Selection

Institutions building behavioral intelligence capabilities should evaluate vendors across four dimensions, treated as sequential filters rather than parallel trade-offs:

**Compliance architecture**, FDCPA/TCPA controls must be embedded at the system level, not bolt-on audit tools. Look for pre-deployment certification workflows and real-time guardrails that block prohibited language before it reaches consumers.

**Behavioral analytics depth**, Platforms should extract structured insights (promise-to-pay intent, financial hardship signals, payment barrier identification) from unstructured conversation data, not just transcription accuracy metrics.

**Integration requirements**, Smooth connectivity to existing CRM, dialer, and payment processing systems determines deployment speed. API-first architectures that support bidirectional data flow reduce the integration tax that kills ROI.

**Conversation quality measurement**, Move beyond first-call resolution rates to evaluate empathy scoring, de-escalation effectiveness, and customer satisfaction proxies that predict long-term payment behavior rather than single-interaction outcomes.

Once you understand the four evaluation dimensions, the next step is to dig into the specific criteria that separate compliant, effective platforms from those that introduce hidden risk.

Key Evaluation Criteria: Compliance, Analytics, and Conversation Quality

Compliance Readiness: Pre-Deployment Vs. Post-Deployment Governance

Most platforms monitor compliance *after* conversations reach customers, transcribing calls, flagging FDCPA and TCPA risks, and scoring adherence once the interaction is complete. That reactive posture catches violations but doesn't prevent them. A smaller set of behavioral intelligence systems stress-test conversation flows *before* deployment, certifying that agents meet disclosure requirements, time-of-day constraints, and mini-Miranda protocol under simulated conditions. Pre-deployment governance generates audit-ready evidence that regulators can review without exposing live customers to untested scripts. When evaluating vendors, distinguish platforms that certify AI behavior upfront from those that only monitor in production, the former reduces the cost and reputational risk of post-contact remediation.

Behavioral Analytics Depth: Beyond Recovery Rates

Volume-only KPIs, recovery rate, right-party contact percentage, tell you *what* happened but not *why* one cohort outperforms another. Behavioral analytics layers payment-history clustering, channel-preference detection, and sentiment awareness onto transaction data. For example, a platform might segment accounts by prior promise-to-pay fulfillment rate and route high-intent borrowers to conversational AI while escalating complex hardship cases to human agents. Real-time strategies and compliance checks surface when an agent deviates from proven negotiation sequences, and post-call analysis extracts settlement opportunities the original script missed. The strategic question is whether a platform quantifies the behaviors that predict sustainable recovery, complaint reduction, repeat engagement, channel migration, or stops at aggregate collection metrics.

Measuring Conversation Quality: Tone, Sentiment, and Complaint Reduction

The market currently proxies human-like interaction through transcript analysis, playbook adherence scoring, and engagement duration, not through standardized linguistic empathy or tone adaptation benchmarks. Academic research confirms the measurement gap: a randomized trial found that borrowers initially contacted by AI agents repaid 1% less of the initial late payment one year later than those reached by human callers, suggesting that nuanced persuasion remains difficult to automate and measure systematically. Vendors highlight resolution rates above 75% and sentiment trajectory analysis, yet these outputs track task completion and emotional tone shift rather than the empathy cues, pausing, acknowledgment phrasing, conditional offers, that build trust. When assessing conversation quality, ask which proxies a platform instruments and whether its analytics distinguish high-engagement dialogues from scripted compliance exchanges.

With compliance and analytics benchmarks established, the question shifts to architecture: which platform type aligns with your institution's volume, case complexity, and risk tolerance?

Platform Categories: Agent-Based Vs. Orchestration-Based Vs. Hybrid Solutions

Agent-Based Voice AI: When to Use Conversational Bots

Agent-based platforms deploy conversational voice bots that handle live calls, IVR automation, and outbound dialing. Tools like ToEbank Collect AI automate payment reminders, negotiate agreements, and authenticate right-party contacts, all with TCPA and FDCPA guardrails embedded. ToEbank reports a 42% promise-to-pay lift and a 35% reduction in agent handle time, positioning agent-based architectures as the high-volume, standardized-call layer. Use voice bots when your portfolio skews toward routine payment arrangements, your team needs 24/7 coverage, and compliance risk is managed through pre-scripted dialogue flows.

Orchestration-Based Platforms: Omnichannel Workflow Coordination

Orchestration systems route conversations across SMS, email, self-serve portals, and voice, coordinating touchpoints rather than conducting them. Text messages achieve a nearly 100% open rate, and nearly 90% of consumers open and read a text within 30 minutes[4], making orchestration the lowest-cost-per-contact layer for early-stage outreach. FICO's omnichannel framework describes this shift from single-channel automation to multi-channel self-service, customers script their journey across digital channels, reducing live-agent dependency. Deploy orchestration platforms when your portfolio spans diverse debtor preferences, you need frictionless channel-switching, and cost-per-contact matters more than call-center throughput.

Hybrid Architectures: Combining Automation and Human Escalation

Hybrid models pair AI-first engagement with human-in-the-loop escalation for complex cases, disputes, hardship negotiations, and third-party disclosure scenarios. Beam AI automates every part of the recovery workflow while allowing teams to collaborate on any step, seeking consent from a live agent when necessary. This architecture delivers the compliance ceiling regulated institutions require: AI handles routine promise-to-pay capture with 100% TCPA/FDCPA coverage, humans resolve edge cases that trigger regulatory scrutiny. Choose hybrid when your portfolio includes high-balance accounts, your compliance team audits every escalation, and your cost structure can absorb selective live-agent involvement. At Domu, we believe orchestration plus selective human oversight is the regulatory safe harbor for CFPB-supervised lenders.

Choosing the right platform architecture means little if it cannot generate audit-ready evidence or pass pre-deployment stress tests, the governance layer that transforms AI from a compliance liability into a defensible asset.

How to Assess Pre-Deployment Governance and Audit Readiness

What Audit-Ready Evidence Means for Risk Committees

Audit-ready evidence in AI collections encompasses conversation transcripts, decision logs, compliance rule triggers, and explainability artifacts that together document how an AI agent reached each customer-facing decision. For risk committees evaluating behavioral intelligence platforms, the CFPB's safe-harbor procedures under Sections 1006.6(d)(4)(i)-(iii) establish the compliance baseline: platforms must document consumer consent, opt-out mechanisms, and disclosure clarity for every email or text interaction.[5] The post-interaction governance gap, where institutions discover compliance violations only after customer harm, drives the shift toward pre-deployment certification. Platforms that generate audit-ready evidence before deployment enable risk committees to review decision logic, flag boundary violations, and produce exam-ready documentation without waiting for production incidents.

Stress-Testing Conversation Flows Before Customer Contact

Pre-deployment testing methodologies, synthetic conversation generation, adversarial scenario simulation, compliance boundary probing, form the governance layer that prevents production violations. Rather than flagging prohibited language after a customer hears it, stress-testing evaluates whether the AI can handle edge cases (third-party disclosure risks, harassment thresholds, cease-and-desist requests) in a controlled environment. The CFPB's chatbot guidance underscores this expectation: customers rightfully expect timely, straightforward answers regardless of the technologies used.[6] Institutions should assess whether a platform supports synthetic testing (can you simulate 1,000 payment negotiation scenarios and review transcripts before launch?), whether it logs decision paths (can you trace why the AI escalated a call?), and whether governance artifacts survive vendor transitions (are logs portable?).

Where Domu Fits: Governance-First Behavioral Intelligence

Domu positions itself within the broader ecosystem by emphasizing pre-deployment governance and audit-ready evidence capabilities. The platform offers formal governance certification for pre-deployment AI approval and provides audit-ready interaction logs for compliance and oversight. Domu's Alex module certifies AI behavior before deployment, stress-testing conversation flows against FDCPA and TCPA boundaries in a synthetic environment. The platform's pros include explainability artifacts for risk committees and behavioral clustering that reveals non-compliant patterns before production launch. Trade-offs: Domu requires integration investment and is not a plug-and-play voice bot. Best-for: institutions with risk committees that prioritize audit-ready evidence and pre-deployment certification over post-deployment monitoring alone. Learn more about Domu's governance philosophy in Redefining a $20B Industry, And Why We're Doing It With Trust.

Even platforms with strong governance capabilities deliver limited value if they cannot exchange data seamlessly with your existing collections CRM and downstream decisioning systems.

Integration Requirements: Connecting Behavioral Intelligence to Your Collections Workflow

Behavioral intelligence platforms promise smarter outreach, but their value depends on smooth data flow between your collections CRM and the AI layer. The integration model you choose determines whether your ops team can deploy insights independently or whether every configuration change requires engineering support.

Api-First Vs. Pre-Built CRM Connectors

Platforms like Skit.ai emphasize fast deployment for lean teams, offering pre-trained collection LLMs and no-code cohort builders that reduce the need for custom API work. This approach suits agencies that want to automate high-volume outreach without maintaining integration pipelines. At the other end of the spectrum, enterprise platforms often require deeper CRM integration investment and may offer richer behavioral clustering along with tools to coordinate servicing workflows. Teams with engineering resources gain custom data pipelines; marketing-led teams gain speed.

Data Flow: Payment History, Contact Preferences, and Real-Time Scoring

Effective behavioral intelligence operates as a two-way street: your CRM must expose payment history, prior contact attempts, and channel preferences via API, while the platform returns debtor scores and next-best-action recommendations in real time. Real-time insights can save significant time and money by reducing uncertainty across collection workflows. Audit whether your collections management system supports bidirectional API calls and whether the platform can write outputs, promise-to-pay flags, compliance alerts, directly back into agent dashboards. Without this loop, insights remain stranded in separate reporting tools, forcing manual reconciliation that erodes the automation benefit.

After evaluating compliance, analytics, governance, and integration, the final filter is use-case fit, matching platform architecture to your institution's operational priorities and portfolio characteristics.

Use-Case Fit: Matching Platform Types to Institutional Priorities

High-Volume Consumer Lending: Agent-Based Automation

When standardized payment plans, low-balance accounts, and call volume drive economics, agent-based voice bots deliver 24/7 coverage without staffing overhead. HubTalk, trusted by 100+ financial institutions, exemplifies this model: script-adherent AI agents handle outbound reminders, payment negotiations, and right-party contact across time zones. Chaseit AI and Floatbot.AI similarly automate IVR workflows for lenders prioritizing throughput over relationship nuance. These platforms fit institutions where baseline recovery rates of 20 to 30% benefit most from persistent, low-cost contact strategies.

Regulated Banking Environments: Orchestration + Pre-Deployment Governance

CFPB-supervised institutions with risk committees require audit-ready evidence before AI agents meet customers. Orchestration platforms that stress-test behavior in staging environments, validating UDAAP compliance, state-specific collection laws, and disclosure accuracy, fit this archetype. Domu issues formal governance certification for pre-deployment AI approval, positioning the platform for banks where the problem was never the rules but proving adherence at scale. Prodigal similarly emphasizes pre-production compliance validation for institutions that cannot afford post-deployment infractions.

B2B and Commercial Collections: Hybrid Human-In-The-Loop Models

Complex commercial accounts, multi-stakeholder negotiation, invoice disputes, relationship preservation, demand hybrid architectures: AI-first engagement with smooth escalation to live specialists. Platforms supporting this model route straightforward payment reminders to agents while flagging high-value or contentious cases for human review. This fit suits lenders managing portfolios where account lifetime value justifies incremental labor cost and where aggressive automation risks client attrition.

Conclusion

Agent-based voice bots deliver 24/7 availability and handle-time reduction but require high call volume to justify investment; orchestration platforms cut cost-per-contact through omnichannel routing but need CRM integration to unlock real-time decisioning. Pre-deployment governance, stress-testing and audit-ready evidence generation, prevents compliance violations before customer contact, while post-deployment monitoring only flags issues in production.

As CFPB oversight intensifies and consumer expectations for empathetic collections rise, the market will shift from volume-only KPIs, recovery rate, right-party contact, to sustainable recovery metrics like complaint reduction, payment plan adherence, and consumer experience. Institutions that adopt pre-deployment governance today will avoid the compliance retrofitting costs competitors will face in 2027-2028.

Audit your current collections workflow against the four evaluation pillars, compliance, analytics, integration, conversation quality, this week, then explore how pre-deployment governance and audit-ready evidence capabilities may fit your institutional priorities.

Frequently Asked Questions

What does 'audit-ready evidence' mean in the context of AI collections tools?

Audit-ready evidence encompasses conversation transcripts, decision logs, compliance rule triggers, and explainability artifacts that document how an AI agent reached each customer-facing decision[5][6]. For risk committees, the CFPB's safe-harbor procedures in Section 1006.6(d)(4)(i)-(iii) serve as the regulatory anchor, platforms must generate these artifacts to satisfy examiner inquiries and internal governance reviews.

How much can AI collections tools reduce operational costs compared to traditional call centers?

Traditional collection operations consume 30-80% of recovery amounts in operational overhead[1][2], and vendors report directional savings within that range. These are vendor-reported estimates, not standardized benchmarks, actual ROI depends on deployment model (agent-based vs. Orchestration), case complexity, and baseline staffing costs. High-volume standardized collections see the most dramatic reductions.

What compliance rules apply to using email and SMS in debt collection?

CFPB Regulation F (effective November 30, 2021) governs electronic communication in debt collection, requiring platforms to support opt-out mechanisms, frequency caps, and unsubscribe tracking[5][6]. Section 1006.6(d)(4)(i)-(iii) establishes three safe-harbor procedures: clear opt-out instructions, limited-content messages, and one-touch unsubscribe links. Platforms must log compliance triggers to generate audit-ready evidence.

Should we choose an agent-based or orchestration-based platform?

Agent-based voice bots automate live calls for high-volume standardized collections, while orchestration platforms route conversations across SMS, email, and self-serve portals at lower cost-per-contact[4]. Nearly 90% of consumers open and read a text within 30 minutes[4], making orchestration efficient for low-touch reminders. Choose agent-based for call-heavy portfolios, orchestration for omnichannel routing.

How do platforms measure conversation quality beyond recovery rates?

The market proxies human-like interaction through post-call transcript analysis, QA playbook adherence scoring, engagement duration, and sentiment flags[3]. Standardized tone adaptation or empathy scoring does not yet exist, academic research confirms the measurement gap. Vendors like Cresta emphasize playbook adherence, while Aryza reports 75% issue resolution as a quality proxy.

What is pre-deployment governance and why does it matter?

Pre-deployment governance stress-tests conversation flows with synthetic scenarios before customer contact, generating audit-ready evidence and certifying compliance boundaries[5][6]. It contrasts with post-deployment monitoring, which only flags violations in production. Platforms like Domu emphasize formal governance certification, a capability competitors often skip, reducing the risk of live FDCPA or TCPA violations.

What recovery rate should we expect from AI collections tools?

Average baseline recovery rates for collections range from 20-30%[3]. Vendor claims report relative improvements, 42% lift (ToEbank), 72% more revenue (Beam AI), not absolute outcomes. Benchmark your current recovery rate first, then assess lift claims against that baseline. Volume-only KPIs tell you what happened but not why one cohort outperforms another[3].

Sources

FDCPA Compliance Checklist: How to Automate Debt Collector - www.ibshome.com

Average Recovery Rates for Collections: Industry Benchmark - www.tratta.io (2025)

AI Debt Collection Software | 40% Higher Recovery Rates - collectdebt.ai

How to Use Email and Text in Your Debt Collection Strategy - PDCflow - www.pdcflow.com

The CFPB's final collections rule: using email and text messages - consumerfinancemonitor.com (2020)

Chatbots in consumer finance - consumerfinance.gov (2023)

10 minutes

Explore Related Articles

GET STARTED

We’re building the next generation of engagement technology: intelligent, automated, and compliant. Our mission is to empower financial institutions to orchestrate every stage of the servicing lifecycle with dignity and unprecedented efficiency.

Supported by

Y Combinator

AWS

Microsoft