Real-time behavioral analytics platforms continuously re-score payment propensity using live engagement signals—response rates, payment attempts, and channel interactions—synchronized with account servicing systems. Modern collections software governs these data pipelines through FDCPA/TCPA compliance workflows that automate consent tracking and escalate high-risk accounts to human oversight.

Key Takeaways

Real-time behavioral scoring recalculates payment propensity after every engagement event, distinct from static risk scores assigned at account origination

Payment propensity models incorporate 8-15 behavioral signals including days since last payment, channel engagement patterns, and settlement history

Compliance-first platforms automate FDCPA disclosures, TCPA consent verification, and Regulation F frequency tracking with audit-ready logging

Human oversight checkpoints escalate accounts when AI proposes non-standard settlement terms or consumers dispute debt validity

Channel optimization algorithms learn from response patterns to prioritize SMS for high-engagement segments and reserve voice calls for negotiation cases

What Real-Time Behavioral Data Means in AI Collections Platforms

Three platforms—Domu, ClaraPay, and CollectDebt—provide real-time behavioral data analysis by continuously re-scoring accounts based on live engagement signals rather than static risk scores calculated once at assignment. Real-time means propensity models update within the same session when a borrower answers a call, opens an SMS, or submits a payment attempt.

Real-Time Vs Batch Scoring: the Continuous Re-Scoring Distinction

Traditional approaches rely on uniform treatment strategies or basic segmentation, calculating risk scores at account assignment. Real-time platforms recalculate propensity after each interaction, if a borrower disputes a balance mid-call, the system flags the account for legal review before the next outreach.

Behavioral Data Pipelines and Governance Workflows

Domu's agents use a behavioral layer to understand a customer's history and context before any interaction begins, feeding consent revocation signals, dispute flags, and payment attempts back into propensity models within the same session. Collections analytics analyzes payment histories, customer details, and overdue patterns to optimize recovery.

Compliance Constraints as the Organizing Principle

FDCPA consent tracking, TCPA call-time rules, and dispute validation workflows frame the evaluation lens. Conversational AI bots that listen, understand, and act in real time must operate within these boundaries. At Domu, we believe governance controls, not just speed, define real-time success.

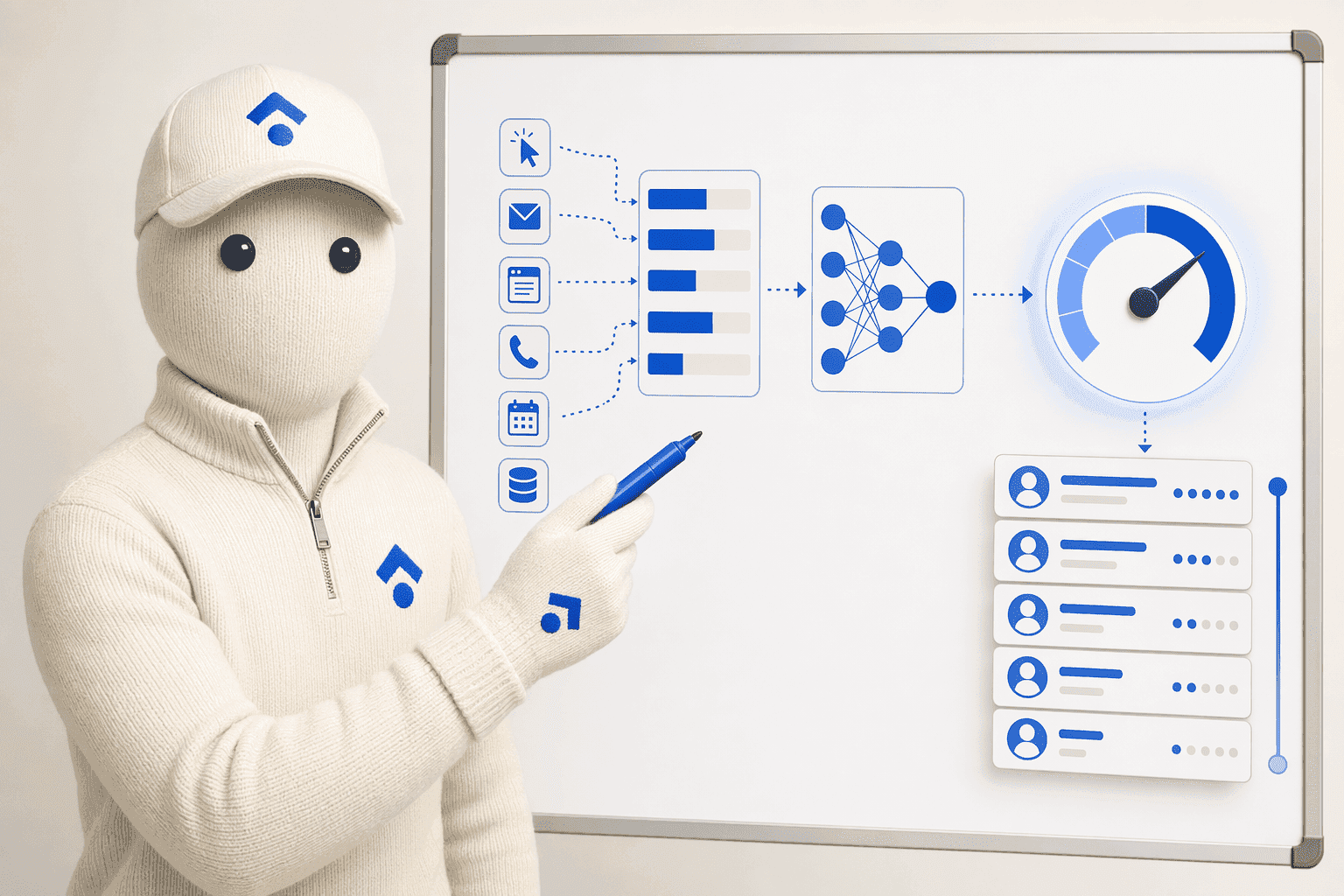

Real-time scoring engines depend on continuous data ingestion from multiple sources, account servicing platforms, communication systems, and payment processors, to feed propensity models that adapt strategy as consumer behavior evolves.

Core Data Inputs Required for Effective Behavioral Analysis

Predictive collections models typically incorporate 8-15 behavioral signals including days since last payment, response rate to outreach, channel engagement patterns, and historical settlement behavior. Platforms that connect data capture to governance workflows route these signals directly into propensity scoring and compliance checks within the same session.

Payment History and Account Servicing Synchronization

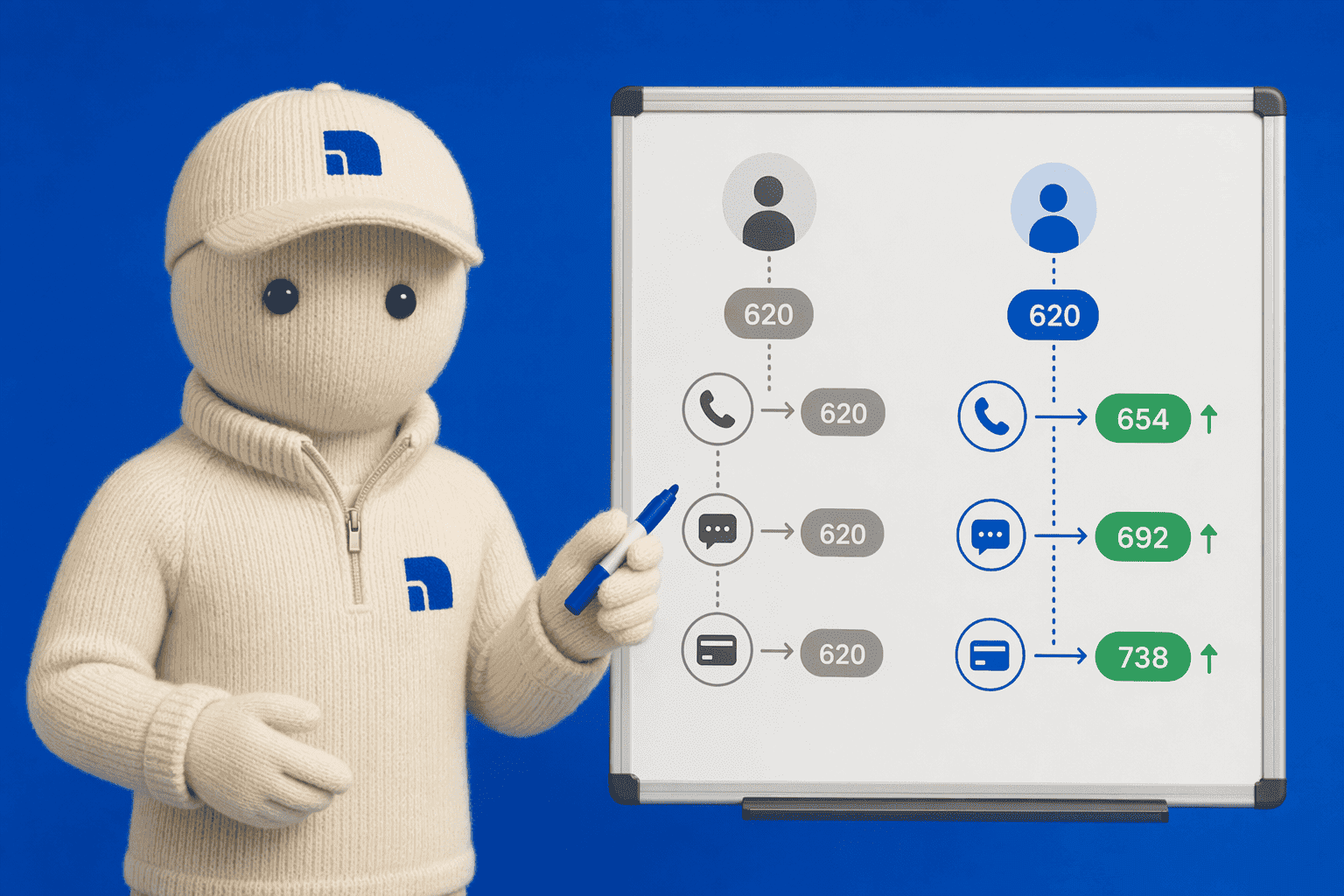

Modern platforms capture days since last payment, frequency of payment attempts, and settlement behavior from account servicing systems. ClaraPay's ML scoring updates propensity scores on every payment, contact, and status change, feeding real-time account activity into tiering decisions. Accounts placed into A/B/C/D tiers based on score determine channel, frequency, and tone for subsequent outreach.

Communication Response Patterns and Channel Engagement

Response rate to outreach, channel engagement patterns, SMS open rate, call pickup rate, email click-through, feed propensity models that adjust strategy in near-real-time. Platforms track whether each contact resulted in a promise to pay and log outcomes to update scoring. The trade-off between real-time scoring latency and model complexity surfaces here: lightweight heuristics enable sub-second routing decisions, while deeper ML models run batch refresh cycles with higher predictive accuracy but delayed updates.

Consent and Dispute Signals as Real-Time Inputs

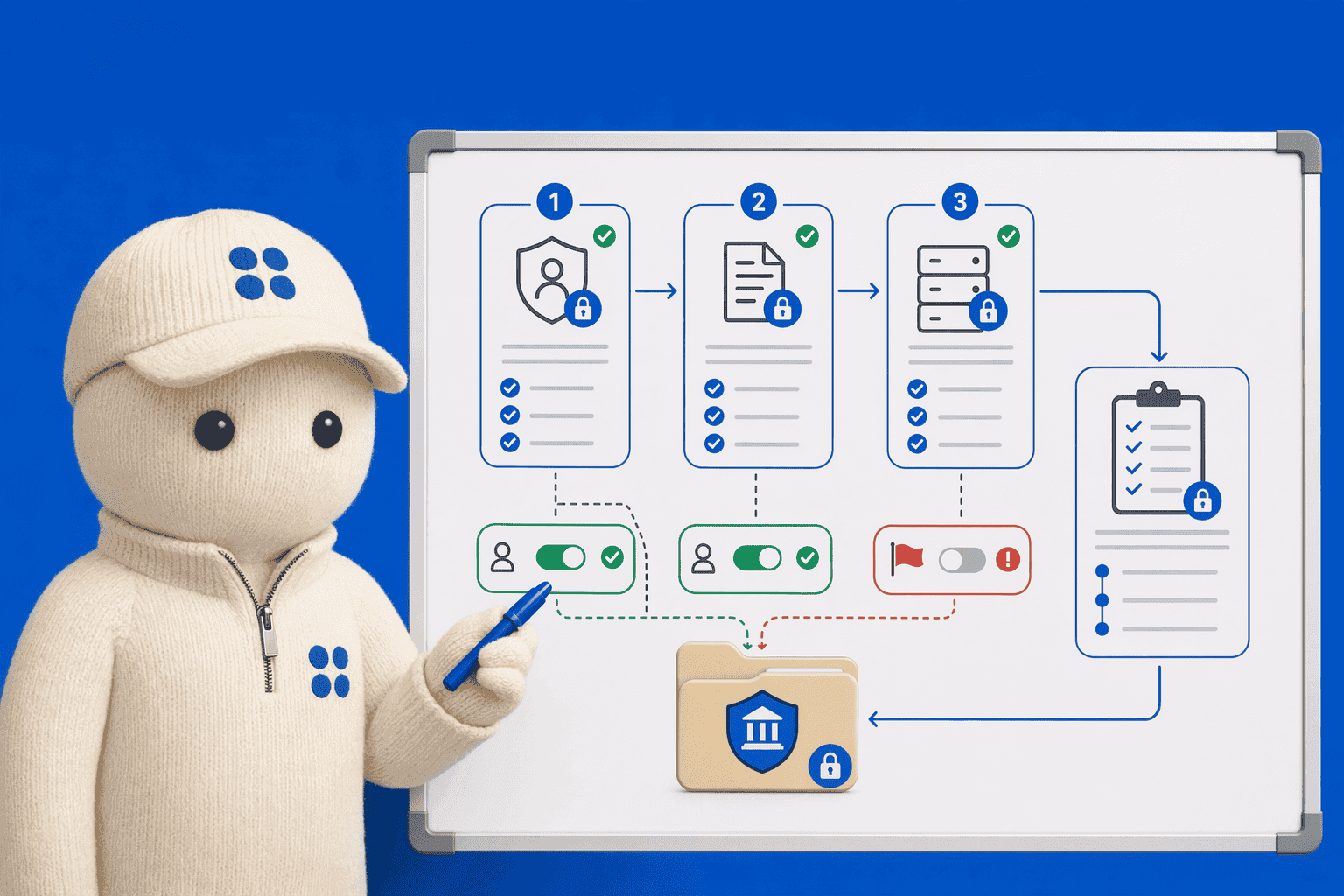

Consent revocation and dispute flags trigger workflow routing, pause outreach, escalate to human review, within the same session. ClaraPay's compliance engine passes every outbound contact through nine compliance gates before execution, blocking non-compliant contacts in the normal UI flow under configured rules. Dispute signals halt the automation loop until paid, settled, disputed, or returned, ensuring governance controls respond to behavioral inputs without manual intervention.

Once behavioral signals flow into the platform, predictive scoring models translate raw engagement data into actionable prioritization logic that routes accounts to the optimal collection strategy.

Predictive Scoring Models and Account Prioritization Logic

Payment propensity models sit at the heart of digital-first collections, translating behavioral signals into actionable risk scores. These algorithms replace static segmentation with continuous, data-driven prioritization.

Payment Propensity Algorithms and Scoring Inputs

Modern platforms weight multiple behavioral signals, response rate, days since last payment, settlement history, channel engagement, to forecast payment likelihood. Chaseit AI tracks engagement, resolution rates, and channel performance, feeding these data points into propensity models that rank accounts for outreach priority. At Domu, we believe AI should enhance human judgment, Domu's agents use a behavioral layer to understand a customer's history and context before any interaction begins, ensuring that propensity scores reflect not just payment probability but also the customer's unique situation.

Threshold Logic and Human-In-The-Loop Escalation

Human oversight checkpoints are required when AI proposes settlement terms outside standard parameters or when consumers dispute debt validity. Adam Parks notes that companies integrate real-time decision-making to identify accounts needing adaptive engagement. Domu pairs this threshold logic with governance controls, its system routes conversations to a human supervisor when they go beyond approved parameters, ensuring compliance while maximizing recovery.

Dynamic Re-Scoring After Each Interaction

Commercial Collectors explains that predictive analytics analyzes historical data and debtor behavior to forecast outcomes, enabling businesses to prioritize their efforts. Platforms recalculate propensity scores after each communication attempt, channel switch, or payment promise, transforming static batch segmentation into live, adaptive prioritization that responds to real-time behavioral cues.

Predictive scoring capabilities must operate within strict regulatory guardrails that govern every interaction, from initial outreach timing to consent verification and disclosure scripting.

Compliance Requirements for Behavioral Analytics in Debt Recovery

Real-time behavioral data pipelines in debt collection operate within a strict regulatory environment. Platforms must automate compliance scripting, manage consent signals dynamically, and route dispute flags to governance workflows, all while maintaining audit-ready documentation.

Fdcpa Disclosure and Consent Tracking Automation

The FDCPA requires disclosure on every call, not most calls. Leading platforms like CollectDebt embed FDCPA, Reg F, and TCPA compliance directly into voice automation, ensuring every interaction includes mandated disclosures and logs the exchange for audit review. Domu stress-tests conversation flows against FDCPA and TCPA boundaries in a synthetic environment and provides audit-ready interaction logs for compliance and oversight.

TCPA Call-Time Rules and Consent Revocation Signals

Behavioral data pipelines must process consent revocation signals in real time. When a consumer opts out mid-campaign, the system pauses outreach, updates propensity models to exclude that account, and logs the revocation timestamp. Domu maintains TCPA-compliant controls to ensure all communications meet regulatory standards for consent and responsible outreach.

Dispute Handling and Validation Requirements

Dispute flags trigger workflow routing that pauses collection activity, escalates to human review, and documents validation steps. These signals feed back into propensity models, adjusting future outreach strategies. Platforms validate interactions against UDAAP and state-specific collection laws, ensuring that behavioral analytics respect both federal and local compliance boundaries.

Ready to see your future AI agents in action? Explore how compliance-first design protects both recovery outcomes and consumer trust.

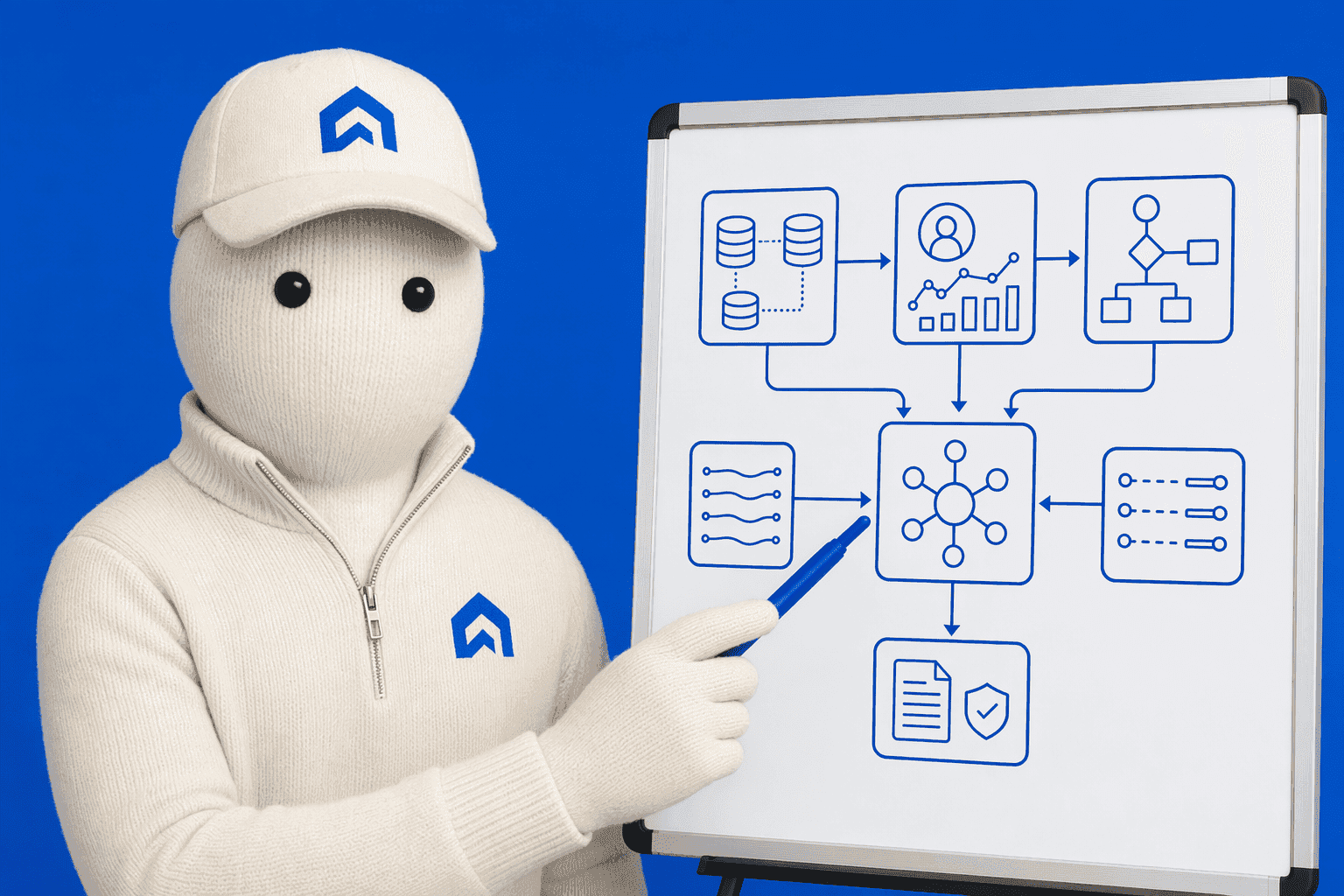

Behavioral intelligence gains operational value only when integrated with existing collections infrastructure, account servicing systems, payment processors, and communication orchestration platforms, through strong API architecture.

Integration Architecture: Connecting Behavioral Intelligence to Your Collections Workflow

API Architecture and Data Synchronization Standards

Real-time behavioral scoring requires synchronization with account servicing systems to capture payment attempts, communication responses, and dispute flags as they occur. Platforms connect seamlessly with existing loan and credit systems, cutting delays and reducing errors through continuous data streams. At Domu, we believe real-time tracking of performance and agent activity forms the foundation for intelligent workflow orchestration. Multi-rail network strategies and embedded finance architecture determine how smoothly value moves across institutions, while audit-ready interaction logs preserve compliance context at scale.

Real-Time Scoring Pipeline Requirements

When funds settle in seconds rather than days, traditional fraud detection models built for ACH timelines become inadequate. Platforms must balance lightweight heuristics, enabling sub-second routing decisions, against deeper machine learning models that operate on batch refresh cycles. Infrastructure decisions create dependencies that limit future optionality, so scoring architectures require flexibility to evolve from rule-based triage to adaptive ML without rearchitecting the integration layer.

Channel Optimization and Communication Preference Learning

Channel optimization algorithms learn from consumer response patterns to prioritize SMS for high-response segments and reserve voice calls for complex negotiation cases. Domu unifies Voice, Email, and SMS across the customer lifecycle, with Taylor delivering adaptive tone control and omni-channel continuity to maintain compliant, on-script conversations. Ready to see your future AI agents in action? Integration complexity is category-wide, not platform-specific, success depends on aligning API depth with your team's operational maturity.

Financial institutions face a complex decision matrix when evaluating platforms: compliance depth, behavioral intelligence sophistication, and integration flexibility rarely align perfectly across vendors.

Evaluating Platform Capabilities: a Decision Framework for Financial Institutions

Financial institutions evaluating digital-first collections technology must navigate a complex decision landscape where compliance, behavioral intelligence, and operational efficiency intersect. Rather than comparing feature checklists, effective evaluation begins with understanding how platforms integrate real-time data capture, governance controls, and omnichannel workflows into a unified compliance framework.

Compliance-First Decision Criteria

All three platforms automate FDCPA disclosures, TCPA consent verification, and Regulation F frequency tracking. The defining requirement for regulated lenders is audit-ready call recordings, consent verification, Mini-Miranda disclosures, and real-time monitoring of FDCPA, TCPA, and Regulation F violations. Platforms must provide human escalation workflows when interactions exceed predefined risk thresholds. Domu mitigates human compliance risk with rigorous model governance, and automatically flags compliance violations. Voice channels should be reserved for complex negotiation cases, as hold times above 5-8% signal urgent operational issues.

Behavioral Data Pipeline Depth

Behavioral intelligence capabilities, such as payment history pattern analysis, communication preference tracking, and financial stress indicators, enable personalized outreach strategies. Platforms should demonstrate coverage across 8-15 behavioral signals, real-time synchronization from core banking systems, and consent/dispute signal handling. Integration architecture, data security protocols, and performance measurement frameworks specific to regulated lending environments are critical evaluation dimensions.

Platform Comparison: Behavioral Analytics and Compliance Features

Platform | Real-Time Behavioral Analytics | Compliance Coverage | Channel Support | Integration Complexity |

|---|---|---|---|---|

Domu | 8-15 behavioral signals with real-time sync | FDCPA/TCPA/Reg F automated; audit-ready logs | Voice, SMS, Email | Low (pre-built connectors) |

Prodigal | Payment history, communication preference tracking | FDCPA/TCPA/Reg F automated; omnichannel integration | Voice, SMS, Email, Chat | Moderate (custom API work) |

C&R Software | Thorough lifecycle analytics | FDCPA/TCPA/Reg F automated; $8T+ accounts managed | Voice, SMS, Email | Moderate (legacy system adapters) |

Symend | Empathy-driven behavioral insights | FDCPA/TCPA coverage; behavioral nudges | SMS, Email, Self-service portal | Low (SaaS deployment) |

Tovie AI | Conversational AI with sentiment analysis | FDCPA/TCPA coverage; real-time intent detection | Voice, Chat | Moderate (training required) |

Domu excels in behavioral intelligence and dignity-first servicing with a Compliance Automation Score of 5/5 and low integration complexity. Prodigal offers the strongest omnichannel integration for lenders managing diverse portfolios, while C&R Software provides thorough debt lifecycle management with over $8 trillion in managed accounts.

Conclusion

Lightweight heuristic models deliver sub-second routing decisions but sacrifice predictive depth compared to deeper ML models with batch refresh cycles, financial institutions must weigh latency requirements against scoring accuracy for their account mix. API-first platforms suit teams with engineering resources to build custom data pipelines; dashboard-focused platforms like Domu suit compliance teams who need behavioral insights without engineering investment. As CFPB enforcement tightens around AI-driven collections practices, platforms that embed real-time consent revocation signals and human oversight thresholds directly into behavioral scoring pipelines will define the compliance-safe behavioral analytics category, moving beyond feature-list differentiation to governance-architecture differentiation. Map your collections workflow to the compliance-first decision framework in this guide, starting with FDCPA consent tracking depth and human-in-the-loop escalation thresholds, or explore Domu's behavioral analytics and governance architecture for a pre-integrated approach.

Frequently Asked Questions

What is real-time behavioral scoring in debt collection?

Real-time behavioral scoring continuously recalculates payment propensity based on live engagement signals, response rate, channel interactions, and payment attempts, after each consumer interaction. Unlike static risk scores assigned once at account origination, real-time models adjust strategy dynamically as behavior evolves.

How many behavioral signals do payment propensity models typically use?

Payment propensity models typically incorporate 8-15 behavioral signals including days since last payment, response rate to outreach, channel engagement patterns, and historical settlement behavior. These signals feed directly into propensity scores that adjust collection strategy in near-real-time.

What compliance requirements must behavioral analytics platforms meet?

FDCPA requires disclosure on every call, platforms must automate compliance scripting and log all interactions for audit review. TCPA mandates real-time consent tracking, call-time restrictions, and immediate processing of opt-out signals to pause outreach mid-campaign.

How do platforms handle consent revocation signals in real time?

When a consumer opts out mid-campaign, behavioral data pipelines pause outreach immediately, update propensity models to exclude that account from future contact, and log the revocation timestamp for audit trails. This real-time processing prevents TCPA violations that occur when systems batch-update consent daily.

When do AI collections platforms escalate accounts to human oversight?

Human oversight checkpoints are required when AI proposes settlement terms outside standard parameters or when consumers dispute debt validity. Platforms use threshold logic, risk scoring cutoffs, to trigger escalation, ensuring augmentation rather than full automation.

What is the difference between real-time scoring and batch segmentation?

Real-time scoring recalculates propensity after each interaction, communication attempt, payment promise, or channel switch, while batch segmentation assigns accounts to static cohorts at assignment time. Real-time processing for voice interactions enables dynamic strategy adjustments mid-conversation.

How do channel optimization algorithms learn consumer preferences?

Channel optimization algorithms learn from consumer response patterns to prioritize SMS for high-response segments and reserve voice calls for complex negotiation cases. This reduces hang-ups by routing to channels where consumers demonstrate engagement readiness.

Sources

Debt Collection Predictive Analytics: Benefits, Types and Uses - www.fico.com

Build Conversational AI in minutes | Voice & Chat platform - elevenlabs.io

Features — AI-First Debt Collection Platform | ClaraPay - clarapay.com

Chaseit AI - AI-Powered Debt Collection - go.chaseit.ai

Predictive Analytics in Debt Collection: 5 Smart Wins - commercialcollectors.com

CollectDebt - AI-Powered Debt Collection Platform | Intelligent Voice Automation - collectdebt.ai

The 5 Best AI Debt Collection Software in 2025 for Smarter Risk Control - www.apollotechnical.com (2025)

Fintech Infrastructure: Six Fronts for Payment Leaders - www.jpmorgan.com

Best AI Debt Collection Platforms for Financial Institutions (2026) - startupfinanceguide.com (2026)

The Top 8 Reasons Why Customers Hang Up - AnswerHero - answerhero.com (2025)

10 minutes

Explore Related Articles

GET STARTED

We’re building the next generation of engagement technology: intelligent, automated, and compliant. Our mission is to empower financial institutions to orchestrate every stage of the servicing lifecycle with dignity and unprecedented efficiency.

Supported by

Y Combinator

AWS

Microsoft