Manual compliance spot-checks review less than 5% of collection communications, leaving systemic FDCPA violations invisible until enforcement actions arrive. Automated monitoring validates every call, SMS, and email against Regulation F timing rules and required disclosures before send.

Key Takeaways

Regulation F limits collectors to seven telephone calls per consumer per week per debt, with automated systems blocking outbound calls when the trailing seven-day window reaches capacity.

Policy-as-checks architecture converts FDCPA Section 807/806 prohibitions into executable validation rules that flag violations for human review before communication send.

Real-time call monitoring detects mini-Miranda disclosure keywords in the first 60 seconds of each call, automating the compliance check that manual QA teams perform post-call.

Omnichannel consent management tracks channel-level opt-in/opt-out status and propagates global cease-communication flags across voice, SMS, and email to prevent exposure.

State-law overlay routing queries consumer jurisdiction and debt origination date to block time-barred collection attempts before outreach occurs.

Understanding Fdcpa and Regulation F Requirements for Collection Communications

Automating FDCPA compliance monitoring requires embedding regulatory constraints—timing limits, mandatory disclosures, consent validation, and validation notice triggers—directly into communication workflows as real-time enforcement checkpoints. Under the Fair Debt Collection Practices Act and CFPB's Regulation F, collection communications are subject to specific requirements that automation systems must validate before, during, and after every consumer interaction.

Regulation F Timing Restrictions: 7-in-7 Rule and Time-Of-Day Limits

Regulation F limits debt collectors to seven telephone calls per consumer per week per debt, with unanswered calls counting toward that total. After seven consecutive failed attempts, the collector must presume the consumer does not wish to communicate via telephone and cease further calls on that debt. Additionally, calls must occur only between 8 a.m. And 9 p.m. In the consumer's local time. Automated systems must track call counts, timestamps, and time-zone conversions in real time to enforce these limits.

Required Disclosures on Every Call: Mini-Miranda and Validation Rights

FDCPA Section 807 requires debt collectors to identify themselves as such in every initial communication—often called the "mini-Miranda" disclosure. Section 809 mandates that consumers receive validation rights notification within five days of the initial communication. Automated voice and text systems must inject these disclosures into scripts and ensure delivery before substantive collection discussions begin. Domu's Alex module stress-tests conversation flows against FDCPA and TCPA boundaries in a synthetic environment to validate that disclosures appear correctly.

Consent Management Across Channels: Fdcpa, TCPA, and State-Law Requirements

Under the TCPA, automated SMS messages require prior express written consent, and every text must include clear opt-out instructions. State laws often impose additional consent or opt-out requirements. Automated systems must maintain a unified consent data model that records consent type (oral, written, channel-specific), timestamp, and revocation status, then checks that model before initiating outreach. Mishandling consent can trigger statutory damages of $500–$1,500 per message.

Validation notice triggers also require automation. Regulation F specifies content and timing for validation notices, including the debt amount, creditor name, and consumer's 30-day dispute window. Systems must generate and deliver these notices within the prescribed time frame and log delivery for audit purposes. Platforms like Domu embed these checkpoints into the servicing lifecycle, treating compliance as an architectural constraint rather than a post-call review step.

Understanding regulatory requirements establishes the baseline — now you need a technical framework that enforces those rules across every communication channel in real time.

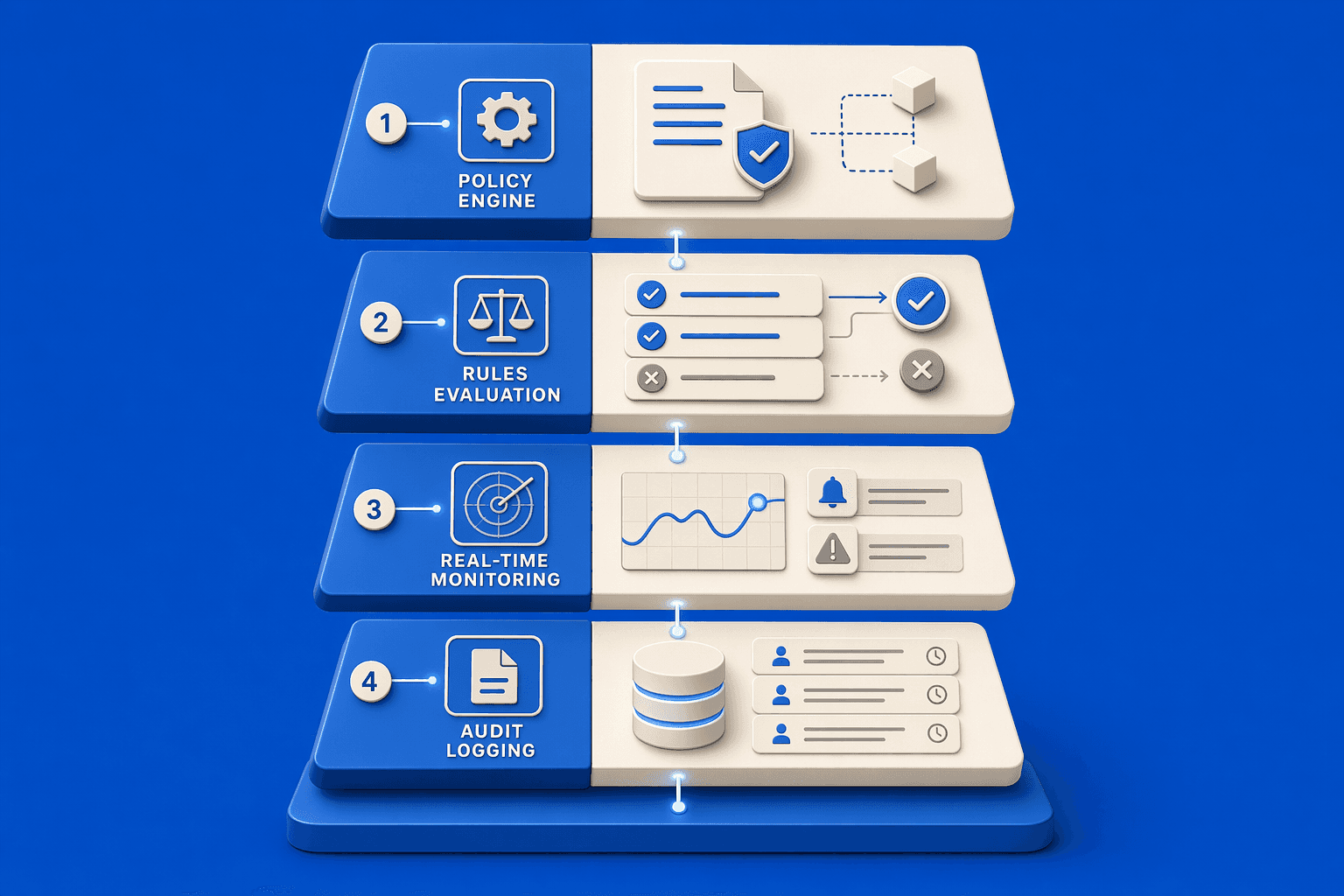

Building Your Compliance Monitoring Framework: Core Components

An effective FDCPA compliance monitoring framework rests on four operational layers working in concert:

Policy-as-Checks Engine — executable validation rules derived directly from FDCPA prohibitions and Reg F timing constraints

Communication Gateway Integration, enforcement points embedded in your dialer and CRM systems that block noncompliant actions before they reach consumers

Audit Trail and Recordkeeping, thorough logs that satisfy CFPB examination standards and provide evidence of every compliance check performed

Escalation Workflow, human-in-the-loop review paths triggered when edge cases exceed automated rule boundaries

Policy-As-Checks Engine: Translating Regulations Into Validation Rules

The policy engine converts FDCPA Section 807/806 prohibitions, false representations, harassment, unfair practices, into executable checks that validate every communication before send. For example, Reg F's seven-in-seven rule becomes a database query: count outbound calls to this consumer in the past seven days; if result ≥ 7, block the attempt and log the enforcement action. Similarly, the mini-Miranda disclosure requirement translates into a script validation check, flag any message that omits the debt collector identification statement.

At Domu, we believe compliance, for an AI agent, isn't a discipline you enforce, it's a constraint built into the architecture. Our system automatically flags violations by validating interactions against UDAAP and state-specific collection laws in real time, ensuring that every validation rule is grounded in policy alignment and regulatory requirements.

Communication Gateway Integration: Enforcing Rules at the Dialer and CRM Layer

The compliance monitoring layer must integrate with your existing dialer and CRM systems to enforce rules at the point of action. When an agent or automated dialer initiates an outbound call, the gateway queries the policy engine: Has this consumer opted out? Does this call violate timing restrictions? Is consent on file for this channel? Only communications that pass all checks are allowed through.

Consider this vignette from Domu's compliance monitoring layer: an agent attempts to place an outbound call to a consumer at 9:15 a.m. Local time on a Tuesday. Before the call connects, the gateway queries the dialer's call history, four outbound attempts in the past six days. The system calculates: one more call today would trigger the seven-in-seven limit tomorrow. The gateway allows the call but flags the account for review, preventing the eighth call from occurring within the restricted window. This integration, not just monitoring after the fact, but enforcement before the action, is what separates compliance automation from compliance theater.

Audit Trail and Recordkeeping: CFPB Examination Standards

Under 12 CFR § 1006.100, debt collectors must retain records that evidence compliance or noncompliance with the FDCPA starting from the date collection activity begins until three years after the last collection activity. This includes call logs, message transcripts, payment histories, and consent forms, not just records of failed communications, but logs of every validation check performed. Domu provides audit-ready interaction logs that capture the complete decision trail, giving compliance teams a reviewable record of every policy validation, every gateway enforcement action, and every escalation trigger.

Ready to see your future AI agents in action? Start a Pilot to explore how Domu's compliance monitoring framework integrates with your existing systems.

The compliance framework enforces timing and consent rules at the gateway level. Real-time call monitoring adds a second validation layer that analyzes agent language and disclosure delivery while the conversation unfolds.

Real-Time Call Monitoring: Automating Fdcpa Disclosure and Language Checks

Live Transcript Analysis: Detecting Missing Disclosures and Prohibited Language

Real-time call monitoring validates mini-Miranda disclosures by detecting keyword patterns in the first 60 seconds of each call, automating the disclosure check that manual QA teams review post-call. Natural language processing scans live transcripts for required phrases ('This is a debt collector,' 'attempting to collect a debt,' 'any information obtained will be used for that purpose') and flags calls where the disclosure is incomplete, delayed, or omitted entirely. Platforms like D1AL detect risky language and abusive phrases as calls happen, while CollectDebt monitors every call, text, or email for FDCPA, TCPA, and Reg F compliance.

FDCPA Section 806 harassment prohibitions, threats, profanity, false urgency claims, serve as the baseline for prohibited language detection. AI flags potential violations (e.g., 'You'll be arrested if you don't pay today') for human review rather than auto-terminating calls. Domu's system detects inappropriate legal language and threats in real time, automatically flagging compliance violations to provide immediate oversight.

Human-In-The-Loop Escalation: When Automated Checks Require Judgment Calls

When a transcript contains language that matches a harassment pattern but the context is ambiguous, 'urgent' versus 'this is urgent or you will be arrested', the system escalates to a supervisor for judgment rather than auto-flagging as a violation. Jordan identifies off-script or unsupported responses in customer interactions for compliance review, analyzing how the AI handled edge cases and confused customers to identify compliance drift. Taylor provides escalation and fail-safe handling alongside on-script enforcement, ensuring conversations remain within approved boundaries while routing ambiguous cases to human oversight. This human-in-the-loop design reflects the principle that AI should enhance human judgment, not replace it blindly.

Call monitoring validates disclosure timing and language during the conversation. Consent management operates upstream, blocking the communication before the agent dials or the SMS gateway sends.

Omnichannel Consent Management: Tracking Preferences Across Voice, SMS, and Email

Consumers interact with brands and businesses across multiple platforms, from emails and text messages to phone calls, and debt collection agencies are no exception. When the FDCPA was passed in 1977, voice calls and letters dominated outreach; today, omnichannel workflows require a unified consent state that reconciles FDCPA cease-communication requests, TCPA prior express consent, and state-specific opt-out triggers across every channel.

Consent Data Model: Reconciling Fdcpa, TCPA, and State-Specific Requirements

Automated systems must track channel-level opt-in/opt-out status (voice, SMS, email), a global cease-communication flag, time-bound consent expiration, and state-specific opt-out triggers. The CFPB updated Regulation F in 2021 to provide guidelines for FDCPA-compliant electronic communications, allowing emails and text messages with direct consent. Yet opt-out notices are required in all electronic communications, must be clear and conspicuous, and the CFPB Small Entity Compliance Guide suggests using a hyperlink or allowing the consumer to reply with words like "stop" or "unsubscribe". Electronic communications must contain all the usual FDCPA and state law disclosures, and messages should generally be sent between 8:00am-9:00pm local time.

Cross-Channel Propagation: Enforcing Opt-Outs When Consumers Request Cessation Via One Channel

Many platforms track consent per channel but do not propagate opt-outs globally, creating compliance exposure when a consumer opts out of SMS but continues to receive voice calls. The contrarian claim: consent must be consumer-centric, not channel-centric. When a consumer requests cessation via one channel (e.g., 'stop texting me' via SMS reply), the system must block ALL channels (voice, SMS, email) unless the consumer explicitly re-consents, the FDCPA Section 805(c) cease-communication requirement applied across modern omnichannel workflows. Platforms like Chaseit AI, which automates conversations across voice, SMS, email, and social media, address this by maintaining unified consent records. Domu's omni-channel communications and TCPA-compliant service similarly reconcile federal and state requirements into a single consent state.

Automated consent management flags risks and enforces rules but does not guarantee compliance, human reviewers must validate edge cases where state law conflicts with federal requirements.

Consent management prevents unauthorized outreach; validation notice workflow automation enforces statutory disclosure timing once the collector makes initial contact.

Validation Notice Workflow Automation and Timing Enforcement

FDCPA Section 809(b) requires a validation notice within five days of the initial communication. Automation must detect the first contact, voice, SMS, or email, and trigger the notice send without manual intervention. Platforms like ClaraPay enforce this by routing every outbound contact through compliance gates that validate timing and content before execution.

Validation Notice Triggers: Automating Initial Communication Detection

The system logs the timestamp of the first consumer contact, flags the account for validation-notice generation, and schedules delivery within the statutory window. This checkpoint prevents collection activity from proceeding until the notice is confirmed sent.

30-Day Dispute Window: Blocking Collection Activity During the Validation Period

Once the validation notice is sent, the platform enforces a 30-day hold on all outbound collection communications. If the consumer disputes the debt, the system automatically blocks calls, emails, and SMS until the dispute is resolved or the validation period closes, ensuring no contact occurs during the statutory window.

Federal FDCPA rules set the compliance floor. State-law overlay routing adds jurisdiction-specific statutes of limitations, garnishment prohibitions, and licensing checks before every communication attempt.

State-Law Overlay Routing and Multi-Jurisdiction Compliance

Federal FDCPA rules establish a compliance floor, but state-specific statutes of limitations, garnishment prohibitions, and licensing requirements create an overlay that varies by the consumer's jurisdiction. Before any collection communication, voice, SMS, or email, platforms must route the request through a state-law compliance layer that checks the consumer's state of residence against three critical parameters: the statute of limitations on the debt, state-level garnishment rules, and whether the collector holds the required license in that state.

Statute of Limitations Enforcement: Blocking Time-Barred Collection Attempts

State statutes of limitations on debt collection range from 3 to 15 years, depending on the debt type and the consumer's state of residence. The routing logic queries two fields, the consumer's current state and the debt origination date, then blocks any communication attempt on time-barred debt. The CFPB's 2024 annual report shows that time-barred collection attempts remain a leading enforcement action driver, positioning statute-of-limitations enforcement as a risk-mitigation layer rather than an optional feature.

Platforms like Syntrove COLLECT encode state-specific statutes into a compliance table that blocks outreach on expired debts automatically. Domu's Jordan module validates customer interactions against state-specific collection laws after deployment, flagging any communication that violates the consumer's state statute of limitations.

Garnishment and Licensing Rules: State-Specific Communication Restrictions

State-level garnishment prohibitions and licensing requirements create additional communication restrictions that overlay federal FDCPA rules. Some states ban wage garnishment for certain debt types; others require collectors to hold an active state license before initiating contact. The routing layer checks the collector's licensing status in the consumer's state and blocks communication if the license is expired or absent.

A common anti-pattern: routing communications by the collector's state of operation rather than the consumer's state of residence. Multi-jurisdiction compliance is governed by where the consumer lives, not where the collector is headquartered. Platforms that fail to key the routing table on consumer state expose their clients to jurisdictional violations that federal FDCPA compliance alone cannot prevent.

Post-Communication QA and Complaint Root-Cause Analysis

Manual spot-check QA reviews less than 5% of collection calls, leaving systemic compliance drift invisible until regulators intervene. Post-communication QA automation closes that gap by analyzing every call transcript, SMS thread, and email exchange to detect patterns, disclosure failures, prohibited language, timing violations, across agent cohorts at scale. When 15% of Agent Cohort A's calls consistently miss the mini-Miranda disclosure or 8% of SMS communications land outside the 8am-9pm window, the system flags the pattern for human review before it becomes a consent-order finding.

Post-Call QA Automation: Detecting Compliance Drift Patterns at Scale

AI transcript analysis operates as a compliance safety net: after each customer interaction, the system parses call recordings and message logs against FDCPA disclosure requirements, TCPA consent boundaries, and Regulation F frequency caps. Domu's Jordan module audits live AI behavior after deployment, identifying policy drift, regulatory risk, and producing regulator-ready evidence from real customer interactions. Jordan analyzes how the AI handled edge cases and confused customers to identify compliance drift, then provides a complete, reviewable record of customer interactions and compliance outcomes.

Where manual QA samples a handful of calls per week, AI-powered platforms validate every interaction against UDAAP and state-specific collection laws. The system identifies off-script or unsupported responses in customer interactions for compliance review, surfacing patterns like repeated failure to verify identity before discussing debt details or inconsistent application of payment-plan eligibility rules. These drift signals move from invisible to actionable within 24 hours rather than waiting for quarterly audits.

Complaint Root-Cause Analysis: Linking Consumer Complaints to Agent Behavior

When consumer complaints spike, post-communication QA connects the dots: the system links complaint data to call transcripts, agent IDs, communication channels, and timing metadata to isolate root-cause patterns. A cluster of "called at work" complaints traced to a single SMS campaign running at 10am reveals a workflow gap, not a platform failure. A surge in "threatened legal action" grievances mapped to three agents using identical off-script language points to training drift in a specific cohort.

This feedback loop mirrors the recovery-rate discipline financial institutions already practice: placing a balance within 90 days can double recovery, while waiting a full year drops odds below 10%. Complaint root-cause analysis applies the same timing pressure to compliance risk, early detection prevents escalation. The analysis identifies whether violations cluster around specific scripts, communication channels (voice versus SMS), or agent tenure cohorts, then routes findings to human reviewers for remediation decisions.

At Domu, we believe post-communication QA operates as a compliance bridge: AI flags risks and elevates patterns to human reviewers, it does not automatically penalize agents or block future communications without human judgment. The system surfaces systemic drift (15% of a cohort's calls missing a required disclosure) faster than manual processes, but the compliance team decides whether the pattern reflects a training gap, a script defect, or an edge-case scenario that merits policy revision rather than enforcement action.

Fully autonomous compliance systems risk blocking legitimate collection outreach when edge cases require judgment, human-in-the-loop escalation workflows balance automation speed with human oversight for ambiguous violations. As CFPB examination standards tighten and state legislatures layer additional consumer protection requirements onto federal FDCPA rules, the compliance monitoring architecture must evolve from feature lists to foundational policy-as-checks layers that validate every communication before send. Explore Domu's compliance monitoring layer to see how policy-as-checks architecture validates collection communications across voice, SMS, and email, or document your current FDCPA compliance baseline and map each regulatory requirement to an automation checkpoint using the framework above.

Frequently Asked Questions

What is the 7-in-7 rule under Regulation F and how do automated systems enforce it?

Regulation F limits debt collectors to seven telephone calls per consumer per week per debt, with unanswered calls counting toward the total. Automated systems query call history before allowing outbound calls, blocking attempts when the consumer has received seven calls in the trailing seven-day window or seven consecutive unanswered calls.

How does automated consent management reconcile FDCPA, TCPA, and state-specific opt-out requirements?

The consent data model tracks channel-level opt-in/opt-out status for voice, SMS, and email, plus global cease-communication flags and state-specific opt-out triggers. When a consumer opts out via one channel, the system blocks all channels unless the consumer re-consents, preventing compliance exposure from siloed consent tracking.

What disclosures must appear in every collection call and how does AI validate them?

FDCPA Section 807 requires debt collectors to identify themselves as such in every initial communication, the mini-Miranda disclosure. Section 809 mandates validation rights notification within five days of initial contact. AI validates these by detecting keyword patterns in the first 60 seconds of call transcripts.

How do automated systems enforce the 30-day validation period under FDCPA Section 809(b)?

When a consumer disputes a debt, the system blocks all collection communications, voice, SMS, email, for 30 days or until the dispute is resolved. The platform enforces this hold automatically after sending the validation notice, ensuring no contact occurs during the statutory validation period.

What state-law overlay checks do automated compliance systems perform?

State statutes of limitations on debt collection range from 3 to 15 years depending on debt type and consumer state. Automated systems query the consumer's state of residence and debt origination date to block time-barred collection attempts, plus state-specific garnishment prohibitions and licensing requirements.

How does post-call QA automation detect compliance drift patterns across agent cohorts?

Manual spot-check QA reviews less than 5% of collection calls, leaving systemic drift invisible until regulators intervene. AI analyzes every call transcript, SMS thread, and email exchange to detect patterns, disclosure failures, prohibited language, timing violations, and elevates findings to human reviewers for root-cause analysis.

What integration requirements do automated FDCPA compliance systems have with existing dialer and CRM platforms?

The compliance monitoring layer must integrate with dialer call history APIs, CRM consent records, and communication gateway send triggers to enforce rules at the point of action. When an agent or automated dialer initiates an outbound call, the gateway queries the policy engine for opt-out status, timing limits, and disclosure requirements.

Sources

Debt Collection Rule (Regulation F) - consumerfinance.gov

12 CFR § 1006.6 - Communications in connection with debt collection. - www.law.cornell.edu

Fair Debt Collection Practices Act - www.ftc.gov

Debt Collector Text Message Regulations - kompatoai.com

1006.100 Record retention. - consumerfinance.gov

Debt Collection Rule Small Entity Compliance Guide - files.consumerfinance.gov (2021)

Understanding Debt Collection and Recovery Options - ACI Worldwide - aciworldwide.com

How Automation is Transforming Compliance in Debt ... - fusioncx.com

What Is Omni-Channel Debt Collection and Why It Matters - www.tecsg.com

Text Messages From Debt Collectors? Not in My Backyard! - www.consumerfinancemonitor.com (2022)

Chaseit AI - AI-Powered Debt Collection - go.chaseit.ai

Debt Collection Rule FAQs - consumerfinance.gov

Features — AI-First Debt Collection Platform | ClaraPay - clarapay.com

CFPB Releases Annual Report on Fair Debt Collection Practices Act FDCPA - www.consumerfinancemonitor.com (2025)

Syntrove COLLECT | Compliance-First Debt Collections Management - www.syntrove.com

Best AI Debt Collection Platforms for Financial Institutions (2026) - startupfinanceguide.com (2026)

10 minutes

Explore Related Articles

GET STARTED

We’re building the next generation of engagement technology: intelligent, automated, and compliant. Our mission is to empower financial institutions to orchestrate every stage of the servicing lifecycle with dignity and unprecedented efficiency.

Supported by

Y Combinator

AWS

Microsoft