Debt collection automation promises efficiency gains, but regulatory compliance must filter vendor shortlists before evaluating cost reduction or conversational quality.

This procurement framework maps four non-negotiable compliance capabilities to three platform categories—orchestrators, analytics overlays, and voice-only solutions—so regulated portfolios can select tools that prevent violations architecturally rather than detect them retroactively.

Key Takeaways

FDCPA compliance architecture—real-time enforcement vs. Post-call audit—must filter vendor shortlists before evaluating voice quality or per-contact economics

Four capabilities are non-negotiable: automated identity verification, real-time 7-in-7 frequency monitoring, Mini-Miranda delivery with confirmation tracking, and dispute escalation protocols

Platform taxonomy maps to buyer scenarios: orchestrators unify omnichannel compliance, analytics overlays add post-call QA to existing systems, voice-only solutions excel at single-channel agent replacement

Total cost of ownership includes implementation timelines (4-12 months), integration labor, ongoing compliance audit staffing, and training overhead beyond per-seat licensing

Phased rollout on pilot cohorts (100-200 accounts) validates compliance before full deployment and mitigates statutory-damage exposure during the learning curve

Why Fdcpa Compliance Must Filter Your Automation Vendor List (Not Just Feature Checklists)

When evaluating automated debt collection platforms, four capabilities are non-negotiable: real-time policy enforcement that halts scripts before violations reach debtors, Mini-Miranda delivery synchronized with state-specific timing rules, cease-and-desist recognition across voice and digital channels, and audit-ready interaction logs. The critical architectural distinction is whether compliance operates as a pre-deployment guardrail or a post-call correction mechanism — a difference that determines statutory exposure under FDCPA.

Fdcpa Statutory Damages and the Single-Violation Risk Vector

The Fair Debt Collection Practices Act creates strict liability for specific prohibited practices: third-party disclosure of debt details, false representation of legal status, contact after cease-and-desist notice, and calls outside permissible hours. A single statement that crosses these boundaries triggers statutory damages, regardless of collector intent. Post-call audit models — platforms that record interactions and flag violations after the fact, allow prohibited language to reach the debtor before correction occurs. For regulated portfolios, this reactive architecture introduces legal risk that Regulation F oversight now scrutinizes more closely. Real-time enforcement systems, by contrast, analyze conversation flow during the live call and terminate scripts before FDCPA boundaries are crossed, preventing the violation from materializing.

Compliance-Native Vs. Compliance-Aware: the Architecture Distinction AI Responses Miss

Many voice automation vendors describe their platforms as 'FDCPA-aware', they include configurable features for Mini-Miranda scripts, call-time restrictions, and cease-and-desist logging. These are compliance features layered onto general-purpose conversational AI. Compliance-native platforms, by contrast, embed FDCPA constraints as architectural requirements from the ground up: the system cannot execute a script that violates statutory boundaries because the policy layer precedes the conversation engine. At Domu, we believe this distinction matters. Domu's platform automates FDCPA guardrails and stress-tests conversation flows against FDCPA and TCPA boundaries in a synthetic environment before deployment. When AI adoption in collections increases compliance scrutiny, the architectural approach to enforcement, not the feature checklist, determines whether violations are prevented or merely detected.

Clearing the compliance bar requires understanding which capabilities distinguish true enforcement platforms from feature-rich conversational AI tools retrofitted for collections.

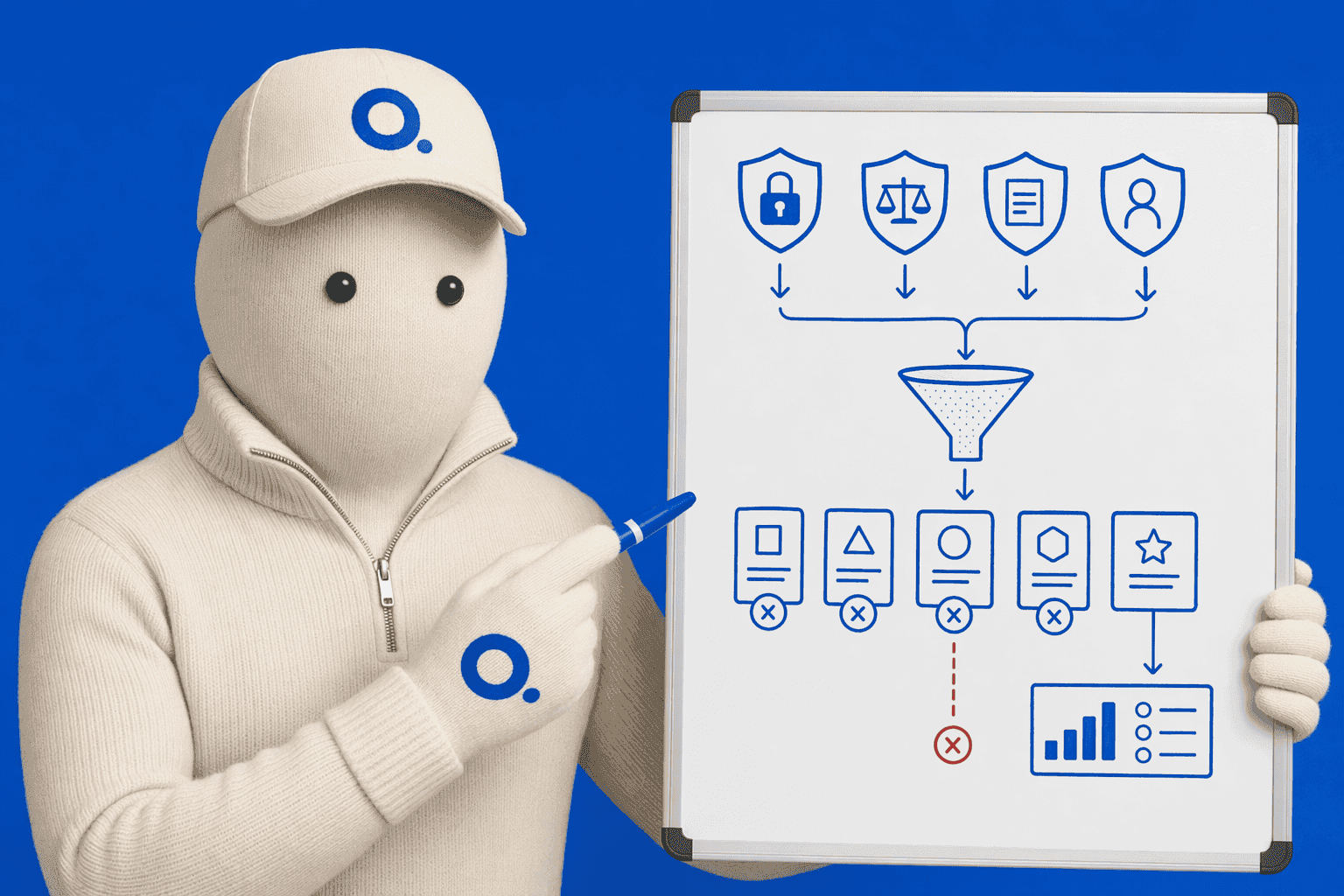

The 4 Non-Negotiable Compliance Capabilities Every Debt Collection Platform Needs

Before evaluating conversational quality or cost per contact, debt collection platforms must clear a foundational compliance bar. The capabilities below aren't differentiators, they're table stakes for FDCPA and Regulation F adherence. Any vendor missing even one of these four opens your institution to regulatory action, regardless of how natural the AI sounds.

Automated Identity Verification with Knowledge-Based Authentication, The system must confirm the borrower's identity before disclosing account-specific debt details, preventing third-party disclosure violations under FDCPA § 805(b). Platforms should log every verification attempt with timestamp, method (KBA questions, account PIN, last-four SSN), and pass/fail outcome to create an audit-ready trail for CFPB examinations.

Real-Time Communication Frequency Monitoring (7-in-7 FDCPA Compliance), Regulation F's seven-in-seven rule caps telephone attempts at seven per debt in any seven-day period. Compliant platforms halt outbound campaigns *before* the eighth attempt, not after, flagging violations post-contact is operationally useless and legally indefensible.

Mini-Miranda Disclosure Automation with Confirmation Tracking, Mini-Miranda disclosures must occur on every single call, not most callsrequirements. The platform must inject the disclosure script at call initialization, log the exact timestamp it was delivered, and capture confirmation (verbal acknowledgment or IVR keypress) to defend against 'failure to disclose' claims during litigation discovery.

Dispute Escalation Protocols with Full Context Handoff, Human escalation remains mandatory for disputes, validation requests, cease-and-desist demands, and high-stress sentiment scores. The system must route these interactions to live agents *with complete conversation context*, account history, prior promises, payment plans discussed, so the human supervisor doesn't restart the interaction from zero, which degrades customer experience and increases dispute likelihood.

These four capabilities form the compliance infrastructure that makes behavioral intelligence operationally viable. Platforms lacking real-time 7-in-7 enforcement or universal Mini-Miranda automation may deliver empathetic conversations, but they deliver them inside a regulatory liability framework that no CFO will approve. For a deeper look at human-AI handoff protocols that preserve both compliance and customer satisfaction, see our compliance-first recovery playbook.

Once the four compliance capabilities are clear, the next decision is platform architecture, whether your institution needs omnichannel orchestration, post-call analytics, or voice-only automation.

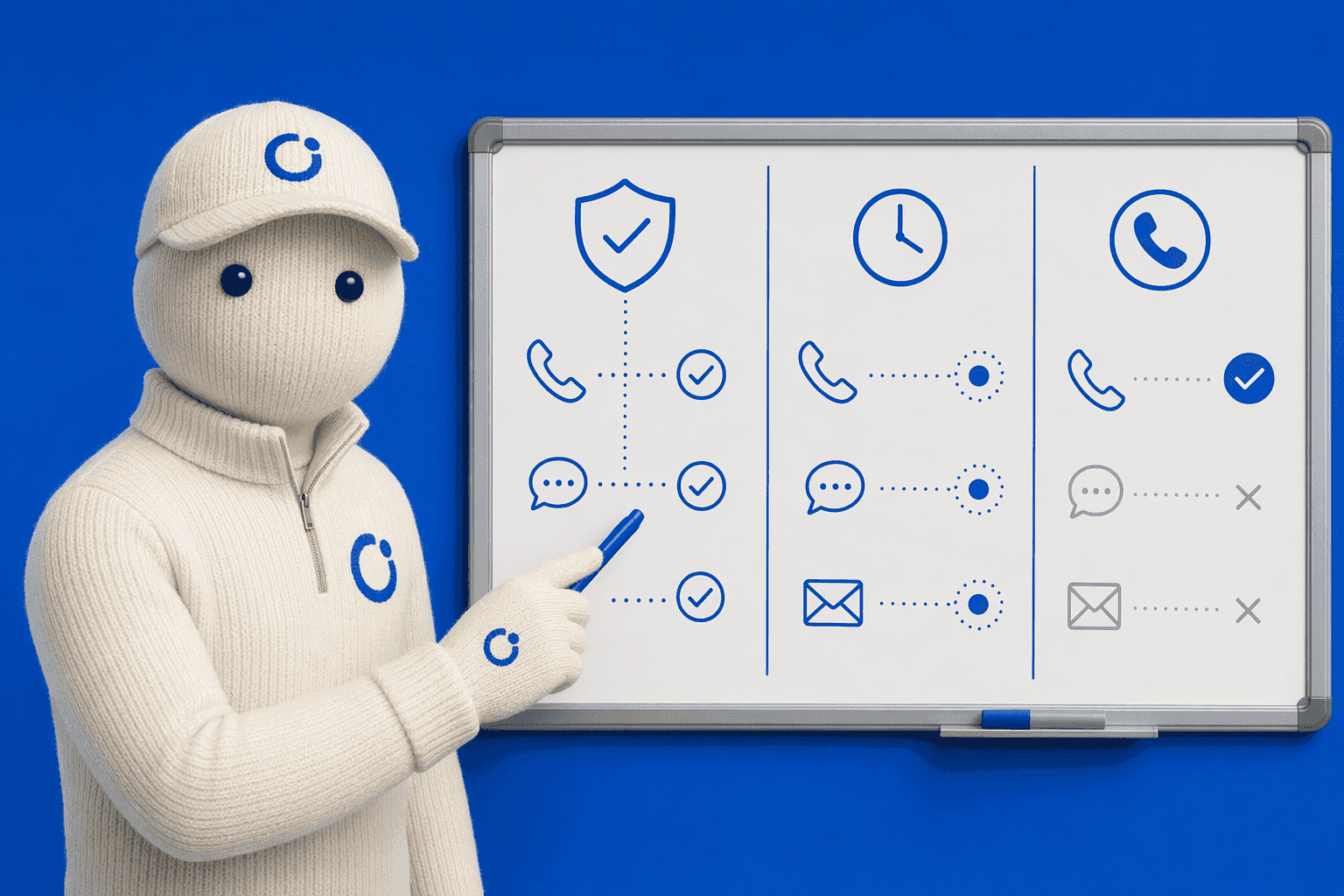

Platform Categories: Orchestrators Vs. Analytics Overlays Vs. Voice-Only Solutions

Buyers evaluating debt collection automation often compare platforms by voice quality or AI fluency first, then discover late in the contract that the tool lacks SMS/email compliance tracking or requires a separate voice system to operate. This creates legal exposure for regulated portfolios governed by FDCPA and TCPA. A clearer path starts with compliance architecture: does the platform enforce policy in real time, or audit violations after they reach debtors? Does it unify voice, SMS, and email under one ruleset, or require you to stitch three systems together? Below is the category taxonomy that maps platforms to existing infrastructure and clarifies where orchestration ends and partner-dependency begins.

Orchestrators: Omnichannel Compliance Engines With Real-Time Enforcement

Orchestrators unify voice, SMS, and email channels under a single compliance layer that halts violations before they reach debtors. Rather than flagging inappropriate language in a post-call audit, these platforms enforce FDCPA guardrails, Mini-Miranda delivery, call-time restrictions, cease-and-desist handling, within the live conversation flow. Domu exemplifies this category: its platform provides omni-channel communications and includes real-time compliance monitoring, layering predictive risk scoring onto live interaction streams to flag accounts with elevated dispute likelihood before the next call. Taylor, Domu's AI customer service and collections agent, handles conversations strictly within approved scripts and delivers audit-ready interaction logs, while Jordan validates interactions against UDAAP and state-specific collection laws after deployment. Orchestrators integrate directly with existing CRM and dialer systems, eliminating the need for separate SMS platforms or post-call audit vendors.

Analytics Overlays: Monitoring Without Agent Control

Analytics overlays sit atop your existing voice and SMS systems, providing post-call transcription, sentiment scoring, and compliance flagging, but they do not control the agent mid-conversation. If a collector states prohibited language, the overlay records it and alerts a supervisor hours later; by then, the violation has already reached the debtor. This reactive model is acceptable for low-stakes service calls but problematic for FDCPA-governed collections where a single prohibited statement can trigger statutory damages. Overlays require separate voice platforms (typically a predictive dialer or cloud telephony provider) and SMS gateways, each with its own compliance configuration. Integration burden is high: buyers must map debtor data across three systems, reconcile transcripts with CRM records, and enforce consistent cease-and-desist logic manually. For teams managing regulated debt portfolios, real-time intervention is the safer architecture.

Voice-Only Solutions: High Voice Quality, No Omnichannel Layer

Voice-only platforms deliver natural-sounding AI calls with strong ASR and TTS but lack SMS/email compliance tracking within the same system. CollectDebt automates recovery using an intelligent voice bot and supports SMS, WhatsApp, email, phone, and chat, positioning itself as multi-channel, yet its behavioral claims center on segmenting accounts and scoring repayment likelihood ahead of a campaign, which is closer to predictive segmentation than real-time adaptation. Retell AI and Floatbot similarly emphasize voice interaction quality but require separate systems for omnichannel campaigns. For FDCPA compliance, voice-only tools depend on script configuration and manual review; they cannot enforce cross-channel guardrails (e.g., halting an outbound SMS if a cease-and-desist was logged during a voice call earlier that day) without custom integration work. Teams using voice-only platforms typically pair them with a compliance overlay or CRM-based workflow engine to close the gap.

Platform | Deployment Model | FDCPA Compliance Features | TCPA/Consent Controls | Call Automation Capacity | Integrations |

|---|---|---|---|---|---|

Domu | Cloud SaaS | Real-time policy enforcement, automated guardrails, audit-ready logs | Consent tracking, timezone-aware call windows, cease-and-desist handling | Thousands of daily calls (Fortune 500 banks, insurers) | CRM, dialer, unified omnichannel |

Retell AI | Cloud API | Configurable scripts, post-call transcription | Manual consent configuration | Not publicly disclosed | Voice-focused, partner-dependent for SMS/email |

Autocalls.ai | Cloud platform | Mini-Miranda delivery, call-time restrictions, cease-and-desist (configured features) | Included for debt collection campaigns | Not publicly disclosed | General voice platform, not purpose-built for financial services |

Floatbot | Cloud SaaS | Not publicly disclosed | Not publicly disclosed | Not publicly disclosed | Multi-channel conversational AI (general-purpose) |

At Domu, we believe compliance architecture should be evaluated before voice quality. An AI that sounds human but lacks real-time FDCPA enforcement exposes regulated portfolios to statutory damages, even if every call is later transcribed and reviewed. Ready to see your future AI agents in action? Start a Pilot to explore how orchestrators like Domu map to your existing infrastructure without requiring separate SMS platforms, post-call audit vendors, or manual cross-channel reconciliation.

Platform category determines how compliance violations are addressed: real-time enforcement prevents prohibited statements from reaching debtors, while post-call audit detects them after statutory damages accrue.

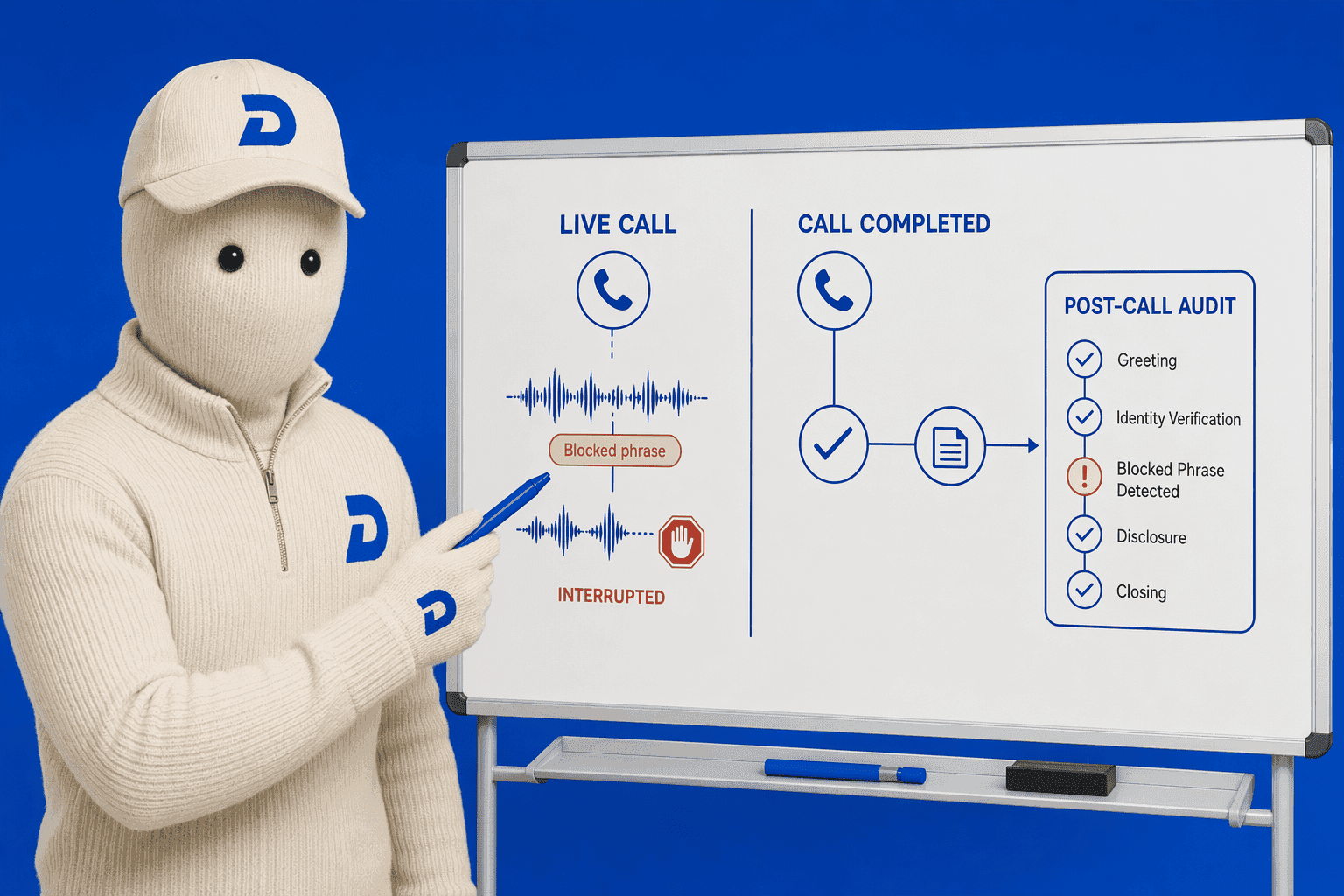

Real-Time Policy Enforcement Vs. Post-Call Audit: Which Model Fits Regulated Portfolios?

Debt collectors face a compliance architecture choice: real-time enforcement that halts script violations before debtors hear them, or post-call audit that detects violations after they occur. The distinction is operational, real-time systems integrate regulatory rules into the agent runtime and interrupt prohibited phrases mid-call, while post-call models run separate QA processes after call completion. This reactive model allows violations to occur and relies on downstream correction, acceptable for low-stakes service calls, problematic for FDCPA-governed collections where a single prohibited statement can trigger statutory damages. For teams managing regulated debt portfolios, real-time intervention is the safer architecture.

Real-Time Enforcement Architecture: How Guardrails Halt Violations Before Debtors Hear Them

Real-time enforcement embeds a regulatory-rule engine directly into the call stack. When an agent begins to utter a phrase that violates FDCPA boundaries, threats, misleading legal language, unauthorized disclosures, the engine interrupts the script, mutes the agent, and either transfers to a human supervisor or terminates the call. CollectDebt.ai positions this as 100% compliant AI debt collection, monitoring every second of every interaction and blocking unauthorized or high-risk calls instantly. Gryphon operationalizes GRC at the point of customer engagement to ensure 100% audit-readiness while eliminating over-suppression of compliant customers. Domu detects inappropriate legal language and threats that violate regulations in real time and automatically flags compliance violations, providing immediate oversight before violations reach debtors.

Post-Call Audit Models: Monitoring Vs. Prevention

Post-call audit platforms record interactions and analyze transcripts after completion, flagging prohibited phrases, tone violations, or missing disclosures for human review. Chaseit describes its AI voice agents as improving over time through A/B testing for performance, which suggests iterative refinement rather than real-time intervention. This model creates a compliance window, between the moment a violation occurs and the moment QA catches it, during which statutory damages accrue. For regulated portfolios, 100% call monitoring does not equal compliance if the monitoring happens after the debtor hears the prohibited statement.

Mapping Compliance Models to Portfolio Risk Profiles

High-volume low-complexity portfolios with in-house compliance teams may accept post-call audit paired with human review, treating violations as training opportunities. Mid-market portfolios benefit from hybrid models, real-time enforcement for high-risk scenarios (threatened litigation, hardship negotiations) and post-call audit for routine payment reminders. Regulated enterprise portfolios require real-time enforcement across all interactions; the litigation exposure from a single FDCPA violation often exceeds the cost of the technology that would have prevented it. 2026 compliance guidance emphasizes that improper SMS content, inadequate documentation, or AI personalization without guardrails can trigger violations, reinforcing the need for runtime controls in digital-first collections.

Understanding enforcement models clarifies the next procurement hurdle: calculating total cost of ownership beyond the per-seat or per-contact pricing advertised in vendor decks.

Evaluating Total Cost of Ownership Beyond Per-Seat Licensing

Pricing Model Comparison: Per-Seat Vs. Orchestration-Layer Vs. Percentage-Of-Recovery

Three pricing models dominate the conversational AI collections landscape. Per-seat licensing bills a flat monthly fee per agent or concurrent session, predictable for teams with stable volume but costly when demand fluctuates. Orchestration-layer pricing charges for API calls, message volume, or conversation count; it scales with usage but can surprise teams during peak collection cycles. Percentage-of-recovery models align vendor incentives with outcomes, taking a share of collected debt; this suits contingent agencies but may increase total cost on high-value portfolios. Each model shifts TCO differently: per-seat favors consistent workloads, orchestration suits variable campaigns, and percentage-of-recovery transfers risk while capping upside for lenders.

Hidden TCO Components: Implementation, Integration, and Compliance Audit Labor

Platform fees represent only part of the total cost. Implementation timelines for enterprise financial institutions typically span three to six months, consuming engineering resources to connect legacy core systems, synchronize consent records across voice, SMS, and email, and train staff on new workflows. Ongoing compliance audit labor, reviewing interaction logs, flagging policy drift, and certifying model behavior against FDCPA and state-specific collection laws, often exceeds initial licensing fees for regulated portfolios. When evaluating vendors, quantify these hidden components: staffing overhead for integration, training cycles, and the recurring audit burden that compliance management platforms require to maintain regulatory confidence.

ROI Variance by Deployment Model and Case Complexity

Vendor-reported savings are not standardized benchmarks; actual ROI depends on deployment model (agent-based vs. Orchestration), case complexity, and baseline staffing costs. A lender moving from call-center agents to AI voice automation may see higher recovery rates if existing processes were manual and reactive, but an agency already using auto-dialers will capture smaller gains. Case mix matters: simple payment reminders automate easily, while hardship negotiations requiring tailored plans demand richer integrations and nuanced scripts. Calculate ROI by modeling your current cost-per-contact, average recovery rate, and the engineering lift required to reach production, not by extrapolating vendor case studies built on different portfolios and tech stacks.

TCO analysis informs budget allocation, but deployment strategy determines whether your institution captures ROI without incurring avoidable statutory-damage exposure during the learning curve.

Implementation Roadmap: Phased Rollout for Risk Mitigation

At Domu, we believe regulated debt-collection deployments demand a low-risk, compliance-validated roadmap, not full-portfolio automation on day one. The three-phase framework below provides a defensible, audit-ready path from pilot to production.

Phase 1: Pilot Cohort Selection and Compliance Baseline (4 to 6 Weeks)

Select a representative subset of 100 to 200 accounts with established payment history and minimal dispute risk. Define success metrics before any conversation takes place: contact rate, promise-to-pay capture, script adherence, and zero FDCPA violations. Autocalls.ai emphasizes pilot-phase contact attempts at $0.03 per interaction, enabling high-volume validation without committing operating budgets to full rollout. Domu offers formal governance certification for pre-deployment AI approval, ensuring every conversation flow is stress-tested against regulatory boundaries before the first debtor call.

Phase 2: Human-Ai Collaboration Model for High-Stakes Scenarios (6 to 8 Weeks)

Define mandatory escalation triggers: disputes, debt-validation requests, cease-and-desist demands, and high-stress sentiment scores above your institution's threshold. AI handles routine payment reminders and self-service arrangements; human agents take over when regulatory risk or customer distress enters the conversation. Floatbot's platform design supports staged agent handoff, a pattern Domu operationalizes through its escalation-path architecture. For a concrete example of on-script enforcement and adaptive tone control during live interactions, see Domu's guidance on maintaining human-like conversations while reducing collection costs.

Phase 3: Full Deployment With Ongoing Audit and Regulatory Review (Post-Pilot)

Expand to larger cohorts only after pilot metrics confirm compliance and recovery lift. Maintain call-recording retention infrastructure and conversation logs for CFPB examination readiness, CrossCheck Compliance notes that expectations around risk management, consumer protection, accountability, and documentation are not new, even when the technology is. Domu automatically flags compliance violations and enforces on-script interactions through its governance certification workflow, providing audit-ready interaction logs for post-deployment review.

Ready to see your future AI agents in action? Start a Pilot with a compliance-validated cohort and human-escalation protocols built in from day one.

Choosing the Right Compliance Architecture for Your Portfolio

Orchestrators like Domu deliver real-time enforcement and omnichannel coverage but require replacing existing voice/SMS systems; analytics overlays preserve your current tech stack but provide post-call audit rather than violation prevention. Voice-only platforms excel at conversational quality and agent-replacement economics but lack the SMS/email compliance layer needed for full Regulation F adherence across digital channels.

As CFPB examination priorities shift toward AI governance and algorithmic accountability in 2026, the distinction between compliance-native platforms and compliance-aware feature sets will become the primary litigation risk vector, procurement decisions made today determine whether your institution defends violations reactively or prevents them architecturally.

Map your portfolio risk profile to the orchestrator/overlay/voice-only taxonomy using the 4-capability checklist from Section 2, then compare Domu's real-time enforcement architecture against your baseline compliance audit burden before committing to a deployment model.

Frequently Asked Questions

Does voice automation guarantee FDCPA compliance?

No, voice automation reduces violation likelihood through AI flagging and real-time guardrails, but human review remains mandatory. Analytics overlays record prohibited language and alert supervisors hours later, meaning violations reach debtors before detection. Real-time enforcement layers halt scripts before violations occur, yet human oversight of dispute escalations and high-stress interactions is still required for full compliance.

What is the difference between real-time compliance enforcement and post-call audit?

Real-time enforcement halts scripts before violations reach debtors by integrating regulatory rules into the agent runtime, preventing statutory damages from accruing. Post-call audit detects violations after they occur through transcription analysis, creating a window where prohibited statements have already been delivered. Competitors often conflate monitoring (detects violations) with enforcement (prevents violations), obscuring this operational distinction.

Which platform category fits my existing infrastructure?

Orchestrators suit institutions building omnichannel compliance from scratch, unifying voice, SMS, and email under a single enforcement layer. Analytics overlays preserve existing voice/SMS systems while adding post-call QA and compliance flagging. Voice-only solutions excel at conversational quality and agent-replacement economics but lack SMS/email compliance tracking required for full Regulation F adherence across digital channels.

How do I calculate total cost of ownership for a debt collection automation platform?

TCO includes platform licensing (per-seat, orchestration-layer, or percentage-of-recovery), implementation timelines (4-12 months for enterprise), integration labor for API/CRM/dialer connectors, ongoing compliance audit staffing, and training overhead. Vendor-reported savings are not standardized benchmarks; actual ROI depends on deployment model, case complexity, and baseline staffing costs. Hidden costs emerge during CRM integration and legacy-system migration.

What are the 4 non-negotiable compliance capabilities every platform needs?

Every platform must provide: (1) automated identity verification with knowledge-based authentication to prevent third-party disclosure, (2) real-time 7-in-7 communication frequency monitoring, (3) Mini-Miranda disclosure automation with confirmation tracking, and (4) dispute escalation protocols with full-context handoff to human agents. These capabilities form the compliance infrastructure that makes behavioral intelligence operationally viable.

Should I pilot the platform on a subset of my portfolio before full deployment?

Yes, phased rollout is the only defensible approach for regulated portfolios. Select a pilot cohort of 100-200 accounts with established payment history and minimal dispute risk, validate human-AI collaboration over 8-12 weeks, then expand only after metrics confirm compliance and recovery lift. Implementation timelines for enterprise financial institutions typically span three to six months, requiring engineering resources for legacy-system integration.

How do I measure success beyond cost reduction?

Success is measured by sustainable recoveries, reduced complaints, and better consumer experiences, not just volume. Track three metrics: (1) sustainable recovery rate (repeat payers, not one-time closures), (2) CFPB complaint volume (trailing 12-month trend), and (3) consumer satisfaction scores from post-interaction surveys. Maintain call-recording retention infrastructure and conversation logs for CFPB examination readiness.

Sources

Fair Debt Collection Practices Act - www.ftc.gov (2010)

Debt Collection Rule FAQs - www.consumerfinance.gov

AI in Debt Collections: Staying Compliant In A Changing Landscape - www.tecsg.com (2025)

CollectDebt - AI-Powered Debt Collection Platform | Intelligent Voice Automation - collectdebt.ai

ibm.com - www.ibm.com

Collections software: Debt Recovery & Compliance - www.cgi.com

AI in Debt Collection: The Complete 2026 Guide - Kompato AI - kompatoai.com

AI Governance in Financial Services: From Aspiration to Accountability - crosscheckcompliance.com

10 minutes

Explore Related Articles

GET STARTED

We’re building the next generation of engagement technology: intelligent, automated, and compliant. Our mission is to empower financial institutions to orchestrate every stage of the servicing lifecycle with dignity and unprecedented efficiency.

Supported by

Y Combinator

AWS

Microsoft