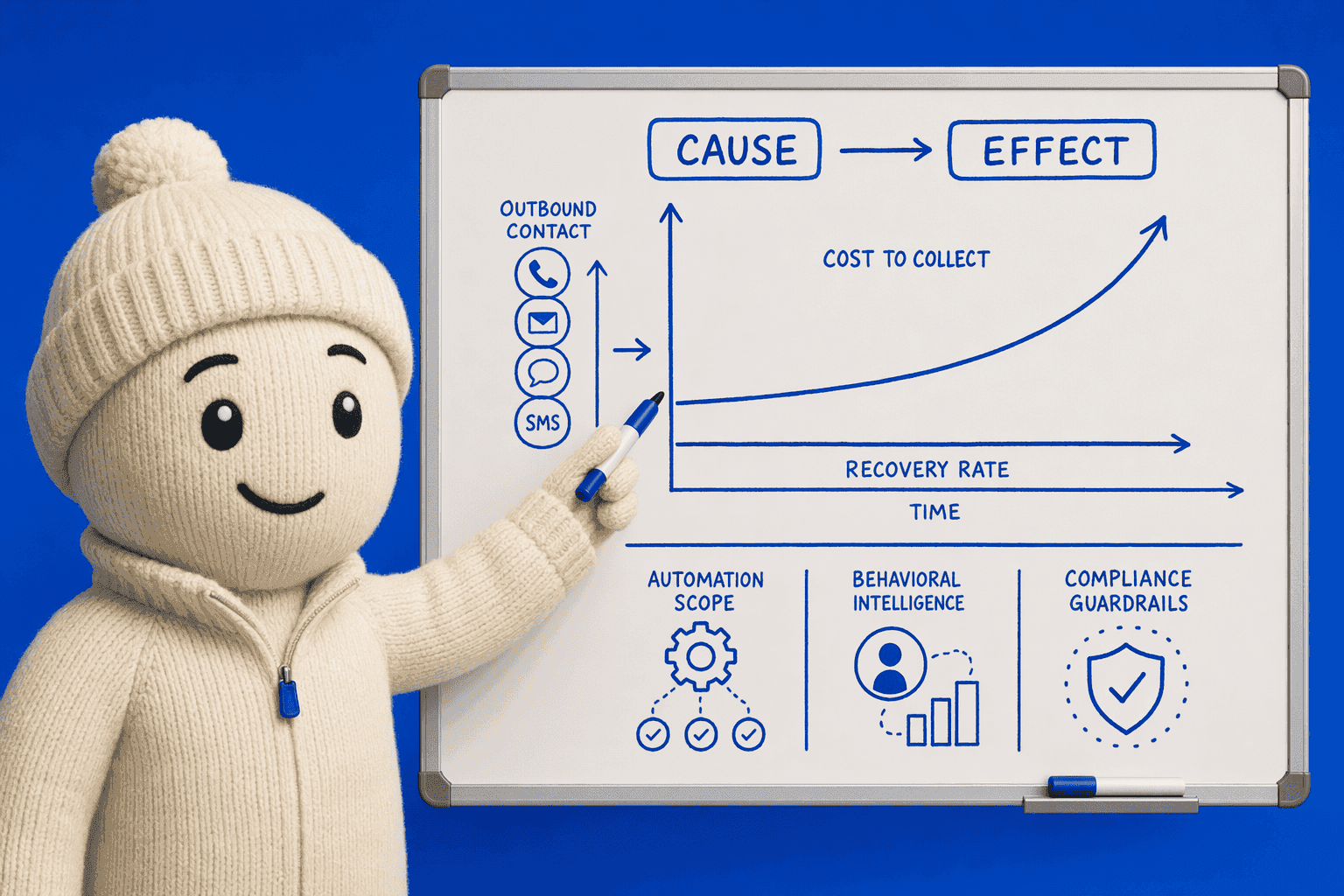

Traditional collections strategies force banks to choose between maximizing recovery rates and controlling operational costs—increasing contact attempts drives up cost-per-account without proportional gains.

Digital-first orchestration platforms break this trade-off by applying selective automation, behavioral intelligence, and compliance guardrails to reduce cost-per-dollar-recovered while maintaining or improving recovery rates.

Key Takeaways

Define clear automation boundaries to separate routine tasks from cases requiring human judgment, ensuring regulatory compliance and operational efficiency

Deploy behavioral intelligence to prioritize high-value accounts and route low-engagement cases away from expensive scoring workflows

Embed real-time compliance guardrails to prevent FDCPA violations that cost up to $1,000 per incident plus legal fees

Measure cost-per-dollar-recovered instead of gross recovery rate to identify where automation delivers ROI and where manual effort is more cost-effective

Implement orchestration platforms that integrate automation scope, behavioral scoring, compliance controls, and cost metrics into a unified operating model

Why Collection Costs and Recovery Rates Move in Opposite Directions

Traditional collections strategies trap banks in a paradox: increasing contact attempts to boost recovery drives up cost-per-account without proportional gains. As delinquency volumes rise and operational budgets face scrutiny, collections teams burn resources on manual workflows—agent calls, handwritten notes, reactive follow-ups—that consume hours per account yet leave recovery rates flat. The answer lies in three operational levers that decouple cost from recovery: automation scope, behavioral intelligence, and compliance architecture.

The High-Touch Trap: Why More Contact Attempts Drive up Cost Without Proportional Recovery

Manual agent-based collections carry hidden overhead: after-call documentation, inconsistent scripting, and sequential account review all erode agent capacity. Industry benchmarks show AI-driven call summarization alone reduces after-call work by 30% and cuts more than one minute from overall call time, yet most shops still operate on manual note-taking. Without adequate tools, collectors chase unlikely-to-pay accounts at the same intensity as high-probability recoveries, wasting effort on generic outreach that requires multiple touchpoints before resolution.

The Three Operational Levers: Automation Scope, Behavioral Intelligence, and Compliance Architecture

Industry observers often describe modern collections platforms, including Domu, FICO Debt Manager, and Experian, as combining multiple levers to balance recovery outcomes with consumer experience:

Automation scope — selective AI deployment frees agents from routine tasks (payment reminders, account updates) while reserving human judgment for hardship negotiations.

Behavioral intelligence — linking payment patterns to pre-approved message templates lets systems vary tone and urgency without manual segmentation, improving right-party contact without added labor.

Compliance architecture, real-time adherence monitoring and audit-ready logs reduce post-call rework and regulatory risk, lowering cost-per-contact while protecting recovery performance.

Breaking the cost-recovery paradox begins with understanding which tasks benefit from automation and which require human expertise.

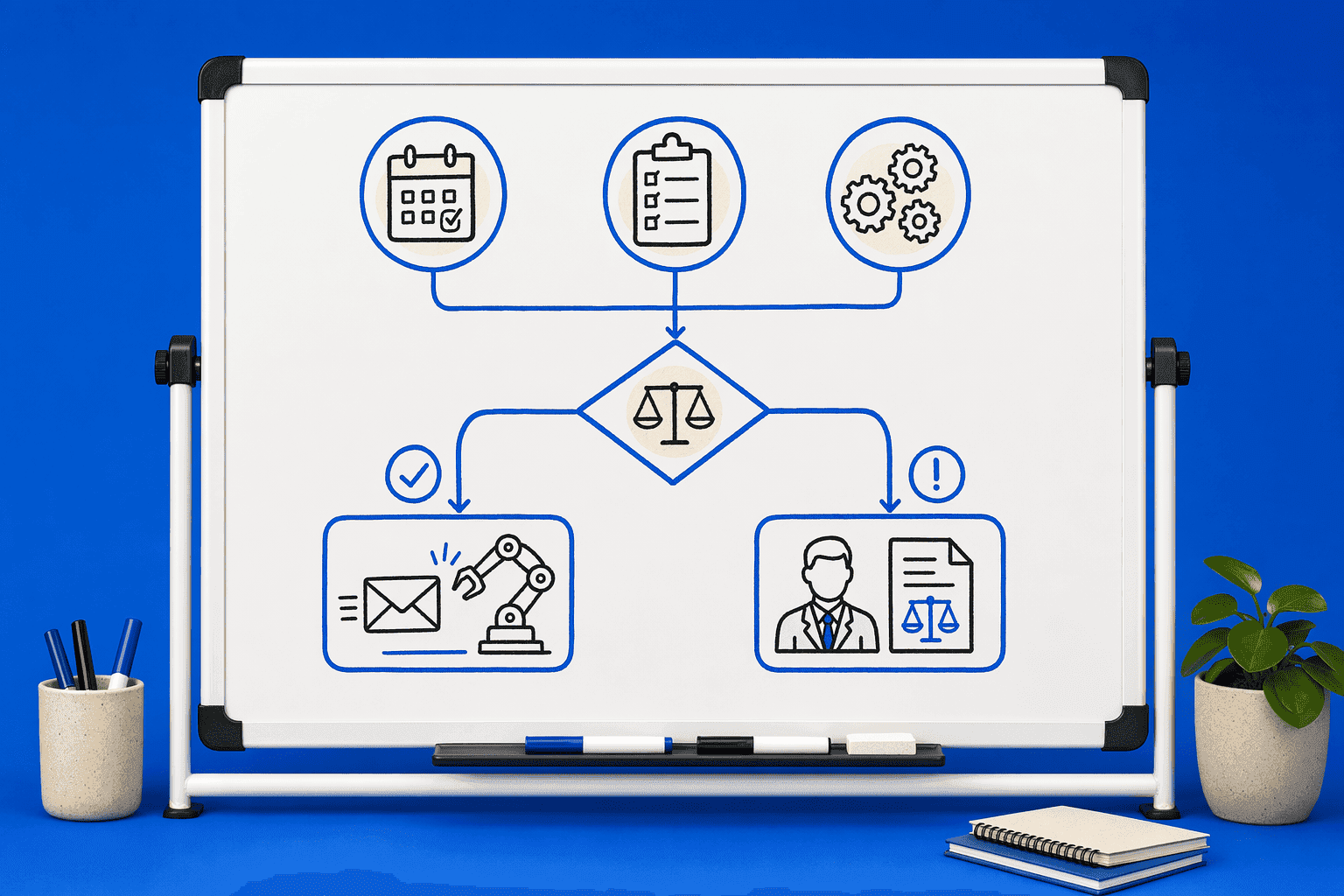

Step 1: Map Your Automation Boundary, What to Automate Vs. Escalate

Before deploying AI voice agents or predictive analytics, define which collections tasks benefit from automation and which require human judgment. This boundary depends on three factors: account age, regulatory surface area, and operational complexity. A 30-day past-due consumer loan reminder is a high-volume, low-risk task that automation handles efficiently. A 180-day account disputing the debt under FDCPA validation rules is a high-risk, low-volume task that demands human oversight and legal expertise.

Automation-Appropriate Tasks: Early-Stage Delinquency and Payment Reminders

Automate tasks where the value proposition is scale, consistency, and 24/7 availability. Early-stage delinquency outreach (30-60 days past due) fits this profile: high contact volume, low regulatory complexity, and standardized messaging. AI-powered platforms analyze vast datasets in real time, predicting borrower behavior and automating compliance. Payment reminders, settlement confirmations, and account status updates are additional candidates, these interactions follow scripted flows, require no negotiation, and benefit from omnichannel delivery across voice, SMS, and email.

At Domu, we believe automation should handle the repetitive work that keeps recovery pipelines moving, freeing human agents to focus on complex cases. Domu's platform is designed with oversight, escalation paths, and controls that keep teams in command. When a situation goes beyond the system's parameters, a human is brought in at the right time and place.

Human-Escalation Tasks: Disputes, Validation Requests, and Negotiation

Certain tasks carry regulatory or reputational risk that automation cannot safely absorb. FDCPA debt validation requests, cease-and-desist demands, payment plan negotiation for hardship cases, and any interaction involving a consumer dispute must remain human-handled. These scenarios require interpretive judgment, empathy, and the ability to navigate ambiguous or adversarial conversations. Real-time flagging is safer for FDCPA-governed collections than post-call audit, a reactive model allows violations to occur and relies on downstream correction, problematic for regulated debt portfolios where a single prohibited statement can trigger statutory damages.

Implementation best practice: route every inbound validation request, every dispute escalation, and every negotiation above a defined dollar threshold to a trained human agent. Domu built a gated tools system requiring human sign-off for some actions, ensuring high-stakes decisions receive approval before execution.

Implementation Sequencing: Which Operational Lever to Address First

Start with automation scope definition before deploying behavioral intelligence or compliance guardrails. Map your portfolio by account age, contact history, and regulatory exposure. Define three tiers: Tier 1 (full automation, routine reminders, confirmations), Tier 2 (automation with human review, settlement offers, payment plans under a threshold), Tier 3 (human-only, disputes, validation requests, negotiation above threshold). This sequencing answers the strategist's knowledge gap on implementation order and ensures you build compliance architecture before scaling contact volume.

There is no one-size-fits-all solution; implementation depends on institution size, portfolio mix, and existing tech stack. A community bank with 5,000 accounts and a single collections team will define a narrower automation boundary than a national credit card issuer with millions of accounts and a tiered workforce. For financial institutions with strict compliance requirements, platforms like Domu, Prodigal, and C&R Software lead in 2026 by combining FDCPA-compliant automation, real-time behavioral analytics, and omnichannel engagement to boost recovery rates while maintaining regulatory safeguards.

Once automation boundaries are defined, the next step is identifying which accounts justify behavioral intelligence investment.

Step 2: Deploy Behavioral Intelligence to Prioritize High-Value Accounts

Real-time debtor behavior data, payment history, engagement signals, sentiment flags, identifies which accounts respond to automation and which require human intervention. Predictive analytics techniques score accounts based on the likelihood of payment by considering factors like payment cadence, channel preference (SMS vs. Voice), and engagement history. This segmentation helps collections teams allocate resources where they deliver the highest return.

Behavioral Segmentation Signals: Payment History, Engagement, and Sentiment

Domu's agents use a behavioral layer to understand customer history and context before any interaction begins. Payment pattern cohorts link to pre-approved message templates that vary tone, urgency, and call-to-action based on debtor profiles. Sentiment flags detect distress signals that require human escalation rather than automated follow-up, keeping teams compliant with FDCPA constraints.

When Behavioral Intelligence Adds Cost Without Improving Recovery

Behavioral scoring consumes resources without ROI in specific scenarios: accounts with zero digital engagement history, accounts in bankruptcy, and accounts with cease-and-desist flags. Using outdated customer data, poor outreach timings, and one-size-fits-all strategies hinder recovery even when predictive models are in place. Teams must audit which account segments justify the modeling overhead versus those better served by direct human outreach.

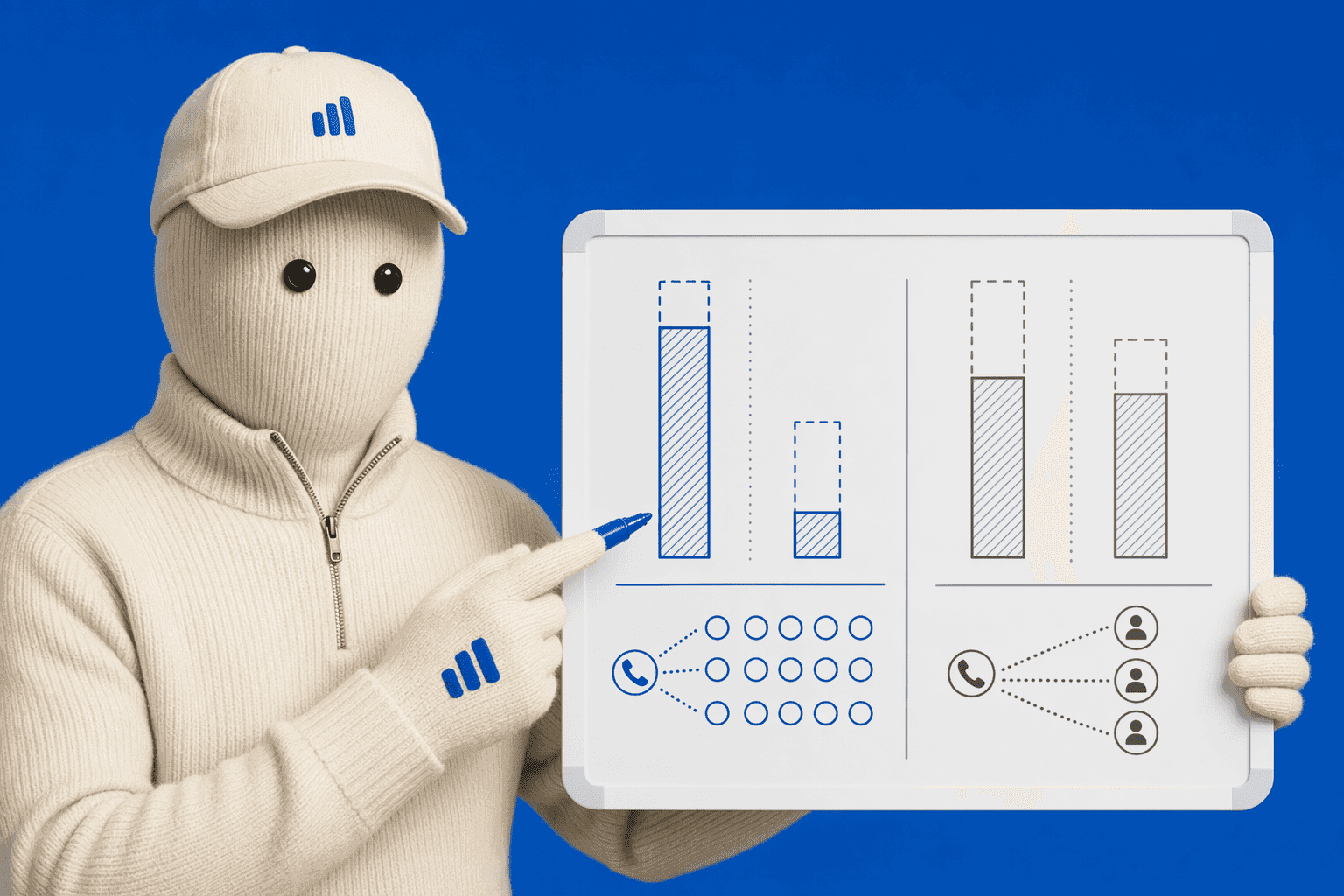

Omnichannel Orchestration: Routing SMS Vs. Voice Vs. Email Based on Debtor Behavior

Behavioral signals drive channel selection and cadence, not rigid rules. Digital-first strategies route debtors who respond to SMS into text-based payment reminders, while accounts with no digital footprint receive voice outreach. This reduces unproductive contact attempts and improves cost-per-dollar-recovered by matching the channel to the debtor's demonstrated preference rather than applying uniform cadences across all accounts.

Behavioral intelligence delivers ROI only when compliance guardrails prevent costly violations from erasing efficiency gains.

Step 3: Embed Compliance Guardrails to Prevent Costly Violations

Fdcpa-Native Guardrails: Mini-Miranda, Cease-And-Desist, and Time-Of-Day Restrictions

Digital collections platforms must enforce mandatory compliance controls in real time to avoid statutory violations. FDCPA-native guardrails include Mini-Miranda disclosure at the start of each call, automatic cease-and-desist handling when a debtor requests no further contact, and time-of-day restrictions that prevent outreach outside 8 a.m. To 9 p.m. Local time. Platforms like CollectDebt are built for FDCPA, Reg F, and TCPA compliance with real-time agent assist, while ElevenLabs delivers low latency interactions with enterprise-grade security to support compliant automation. Domu's platform automates these FDCPA guardrails, removing the manual burden and allowing agents to concentrate on empathetic communication.

Compliance Violation Cost Exposure: Statutory Damages Under Fdcpa

Each FDCPA violation exposes financial institutions to statutory damages up to $1,000 per individual claim, plus attorney's fees and court costs. For class-action suits, damages can reach the lesser of $500,000 or 1% of the creditor's net worth. Preventing a single violation through automated guardrails can pay for the compliance architecture investment, framing real-time controls as a financial risk-mitigation priority rather than overhead.

Compliance Architecture Requirements for Banks Vs. Third-Party Agencies

In-house bank deployments face CFPB oversight and higher regulatory scrutiny than third-party agencies, requiring stricter audit trails and escalation rules. Modern collections software must maintain compliance with regulatory standards while consolidating data from multiple systems. Automated guardrails prevent the majority of violations, but edge cases, dispute validation, payment plan negotiation, still require human legal review. Human oversight remains mandatory; AI alone cannot guarantee FDCPA compliance.

Compliance controls protect margin, but sustainable cost reduction requires measuring the right efficiency metric.

Step 4: Measure Cost-Per-Dollar-Recovered, Not Just Recovery Rate

Why Gross Recovery Rate Misleads: the Hidden Cost of High-Contact Strategies

Gross recovery rate, percentage of delinquent dollars collected, incentivizes high-contact-volume strategies that inflate operational costs without proportional recovery gains. A 70% recovery rate achieved through fifteen outbound calls per account is operationally unsustainable compared to a 65% rate achieved through three targeted contacts. Measuring recovery alone hides the efficiency trade-off: volume-driven outreach drives up cost-per-account faster than it lifts recovery dollars.

Calculating Cost-Per-Dollar-Recovered: Operational Costs Divided by Recovered Amount

Cost-per-dollar-recovered measures the total expense required to recover delinquent accounts, including staff time, technology costs, communication expenses, and administrative overhead. The formula is straightforward: divide total collections operating costs by total dollars recovered in the same period. A collections operation spending $50,000 per month to recover $500,000 has a cost-per-dollar-recovered of $0.10. Lowering that figure, through selective automation on high-volume, early-stage accounts, directly improves profitability on every loan product.

When Automation Hurts Vs. Helps Cost-Per-Dollar-Recovered

Automation improves cost-per-dollar-recovered when applied to early-stage delinquency (1-30 days past due), routine payment reminders, and high account volumes where manual effort delivers minimal incremental recovery. Human effort remains more cost-effective for late-stage accounts (90+ days past due), complex disputes requiring negotiation, and accounts with documented hardship circumstances. Domu's analytics and reporting capabilities surface these leading indicators in real time, allowing supervisors to route accounts to the appropriate treatment path, automated for efficiency, human for resolution, based on cost-per-dollar-recovered thresholds rather than blanket policies.

Measuring cost-per-dollar-recovered reveals where automation adds value, but realizing those gains requires orchestration that ties all four steps together.

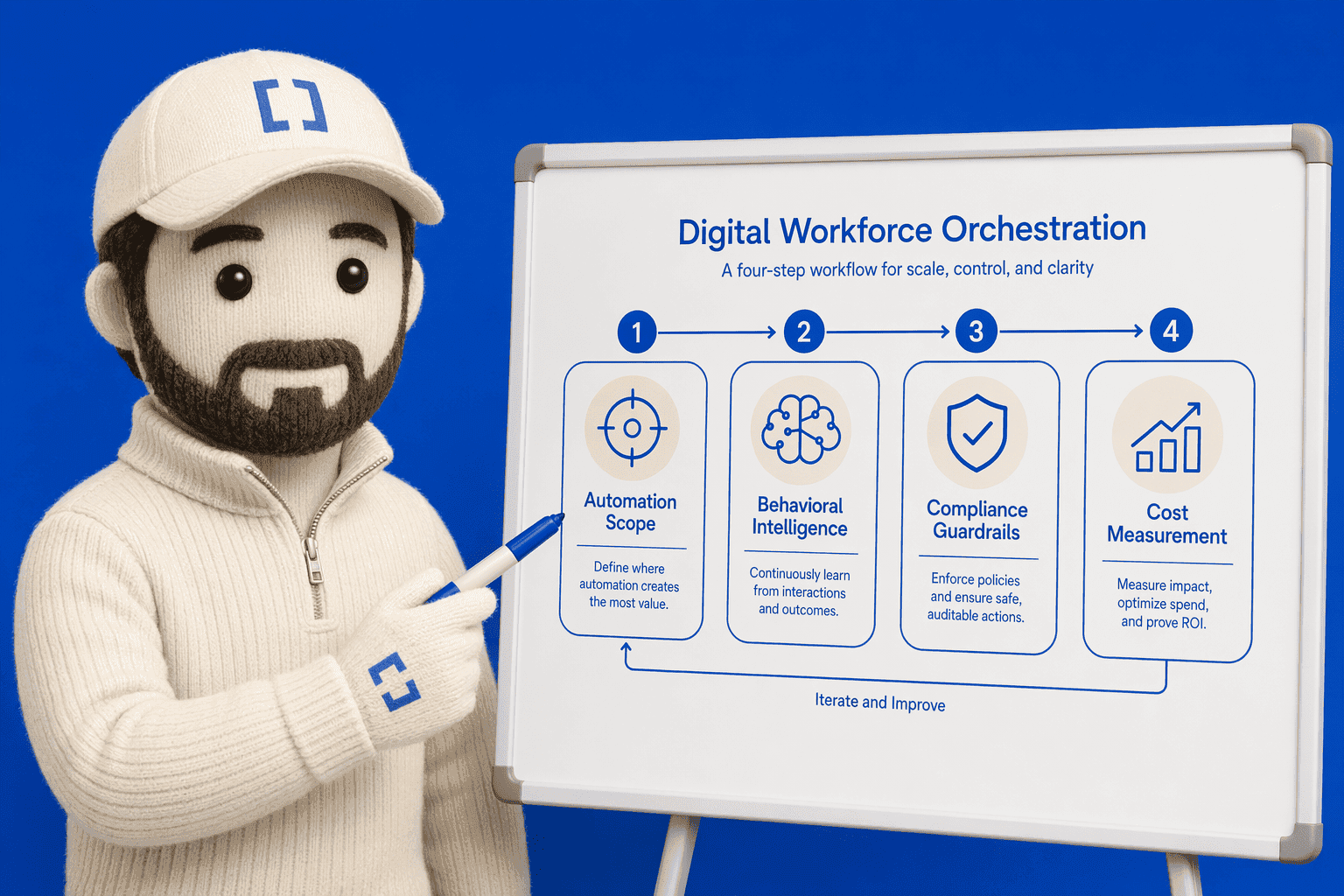

How Digital-First Orchestration Platforms Reduce Cost While Maintaining Compliance

At Domu, we believe orchestration is not a feature, it's the workflow that ties automation scope, behavioral intelligence, compliance guardrails, and cost measurement into a single operating model. When collections teams ask how platforms reduce cost while maintaining compliance, they are really asking how these four steps integrate in practice.

Orchestration Model: How the Four Steps Integrate in Practice

The operational workflow begins with automation scope decisions: which accounts qualify for AI-driven outreach, which require human judgment, and which channels (voice, SMS, email) to activate. That scope drives behavioral prioritization, segmenting accounts by propensity to pay, preferred contact time, and communication history. Behavioral signals then trigger compliance guardrails: Domu automatically flags compliance violations and enforces on-script interactions through its governance certification workflow, ensuring that every automated touchpoint stays within FDCPA boundaries. Finally, cost-per-dollar-recovered measurement closes the loop, feeding operational cost data (agent hours saved, call volume reduced) and recovery outcomes back into the scope decision for the next cycle.

Other platforms demonstrate different orchestration architectures: Chase It AI emphasizes 24/7 continuous engagement across voice, SMS, email, and social media, with compliance adherence built into the workflow. ClaraPay offers a feature-rich orchestration layer that integrates debtor communication across multiple touchpoints. Each platform balances the same four levers, automation boundary, behavioral intelligence, compliance enforcement, and cost measurement, but with different operational trade-offs.

Automation ROI Timelines: When Savings Materialize by Deployment Model

Cost savings do not appear instantly. These are vendor-reported estimates, not standardized benchmarks, actual ROI depends on deployment model (agent-based versus orchestration), case complexity, and baseline staffing costs. Agent-based models (where AI handles routine calls and escalates edge cases to human collectors) typically show measurable cost reduction within the first quarter as call volume drops and agent time shifts to high-value accounts. Orchestration models (where the platform routes tasks dynamically across AI and human workflows) require longer integration timelines, usually two to three quarters, before operational cost savings materialize, because the upfront work involves mapping existing workflows, training the AI on institutional compliance policies, and fine-tuning escalation rules.

As CFPB oversight tightens and statutory damages rise, the industry is shifting from AI-first to compliance-first orchestration models that treat guardrails as a cost-saver rather than overhead. Platforms that automate FDCPA compliance checks, like Domu's approach to removing the manual burden of compliance monitoring, reduce the operational risk that historically required dedicated QA teams to review every agent interaction. That shift turns compliance from a cost center into an efficiency lever.

Ready to see your future AI agents in action? Start a Pilot to integrate orchestration, compliance automation, and cost measurement into your collections workflow.

Conclusion

Single-platform solutions like Domu reduce integration complexity but may offer less customization than API-first tools like FICO Debt Manager, choose based on whether your team prioritizes speed-to-value or workflow flexibility. Cloud-based deployment accelerates ROI timelines but may require vendor-managed compliance updates; on-premise solutions offer more control but slower implementation and higher IT overhead.

As CFPB oversight intensifies and statutory damages rise, the collections industry is shifting from AI-first to compliance-first orchestration, where real-time guardrails prevent expensive violations rather than treating compliance as overhead, and cost-per-dollar-recovered replaces gross recovery rate as the primary efficiency metric.

Get a free baseline assessment of your current cost-per-dollar-recovered using Domu's compliance-first orchestration platform, or explore the knowledge base to map your automation boundary before deployment.

Frequently Asked Questions

What is the typical cost-per-contact difference between manual and automated collections?

Manual agent-based collections include hidden overhead like after-call documentation, inconsistent scripting, and sequential account review. Industry benchmarks show AI-driven call summarization alone reduces after-call work by 30% and cuts more than one minute from overall call time.

When should we escalate a collections case to a human agent instead of using automation?

FDCPA debt validation requests, cease-and-desist demands, payment plan negotiation for hardship cases, and any interaction involving a consumer dispute must remain human-handled due to regulatory risk that automation cannot safely absorb.

How much do FDCPA violations cost per incident?

Each FDCPA violation exposes financial institutions to statutory damages up to $1,000 per individual claim, plus attorney's fees and court costs. As CFPB oversight tightens, compliance-first orchestration models treat guardrails as a cost-saver by preventing violations rather than treating compliance as overhead.

What recovery rate benchmarks should we expect for early-stage vs. Late-stage delinquency?

Automation improves cost-per-dollar-recovered when applied to early-stage delinquency (1-30 days past due) and routine payment reminders. Human effort remains more cost-effective for late-stage accounts (90+ days past due) where negotiation and context matter more than speed.

How long does it take to see ROI from collections automation?

Cost savings do not appear instantly. Vendor-reported estimates vary based on deployment model (agent-based versus orchestration), case complexity, and baseline staffing costs. Actual ROI timelines depend on whether the platform is cloud-based or on-premise.

Can AI alone ensure FDCPA compliance in collections?

Automated guardrails prevent the majority of violations, but human legal review remains mandatory for edge cases like disputes, validation requests, and cease-and-desist handling. In-house bank deployments face CFPB oversight requiring stricter audit trails and escalation rules.

What is cost-per-dollar-recovered and how do we calculate it?

Cost-per-dollar-recovered equals operational costs divided by recovered amount. A 70% recovery rate achieved through fifteen outbound calls per account is operationally unsustainable compared to a 65% rate achieved through automated sequences, making cost-per-dollar-recovered a better efficiency metric than gross recovery rate.

Sources

The seven pillars of (collections) wisdom - www.mckinsey.com (2018)

Reducing Cost-to-Collect in Mid-Sized Banks While Improving Cure Rates with Intelligent Collections - www.businessnext.com

AI in debt collections: 3 use cases that move KPIs - www.cgi.com

The 5 Best AI Debt Collection Software in 2025 for Smarter Risk Control - www.apollotechnical.com (2025)

Best AI Debt Collection Platforms for Financial Institutions (2026) - startupfinanceguide.com (2026)

Debt Collection Strategies: The Definitive Guide for 2026 - moveo.ai (2026)

Chaseit AI - AI-Powered Debt Collection - go.chaseit.ai

Features — AI-First Debt Collection Platform | ClaraPay - clarapay.com

10 minutes

Explore Related Articles

GET STARTED

We’re building the next generation of engagement technology: intelligent, automated, and compliant. Our mission is to empower financial institutions to orchestrate every stage of the servicing lifecycle with dignity and unprecedented efficiency.

Supported by

Y Combinator

AWS

Microsoft