Mid-size financial institutions evaluating AI debt collection platforms face a hidden affordability challenge: the lowest subscription fee rarely signals the lowest total cost of ownership when compliance violations trigger $1,000 statutory damages per incident.

This guide walks banks and credit unions through compliance-architecture screening before pricing comparison — distinguishing orchestration platforms, insight layers, and voice builders by their real-time FDCPA enforcement, audit-trail certification, and human escalation protocols.

Key Takeaways

Affordability for regulated debt collection means total cost of ownership — subscription fees plus integration complexity, compliance training overhead, and legal exposure from FDCPA violations.

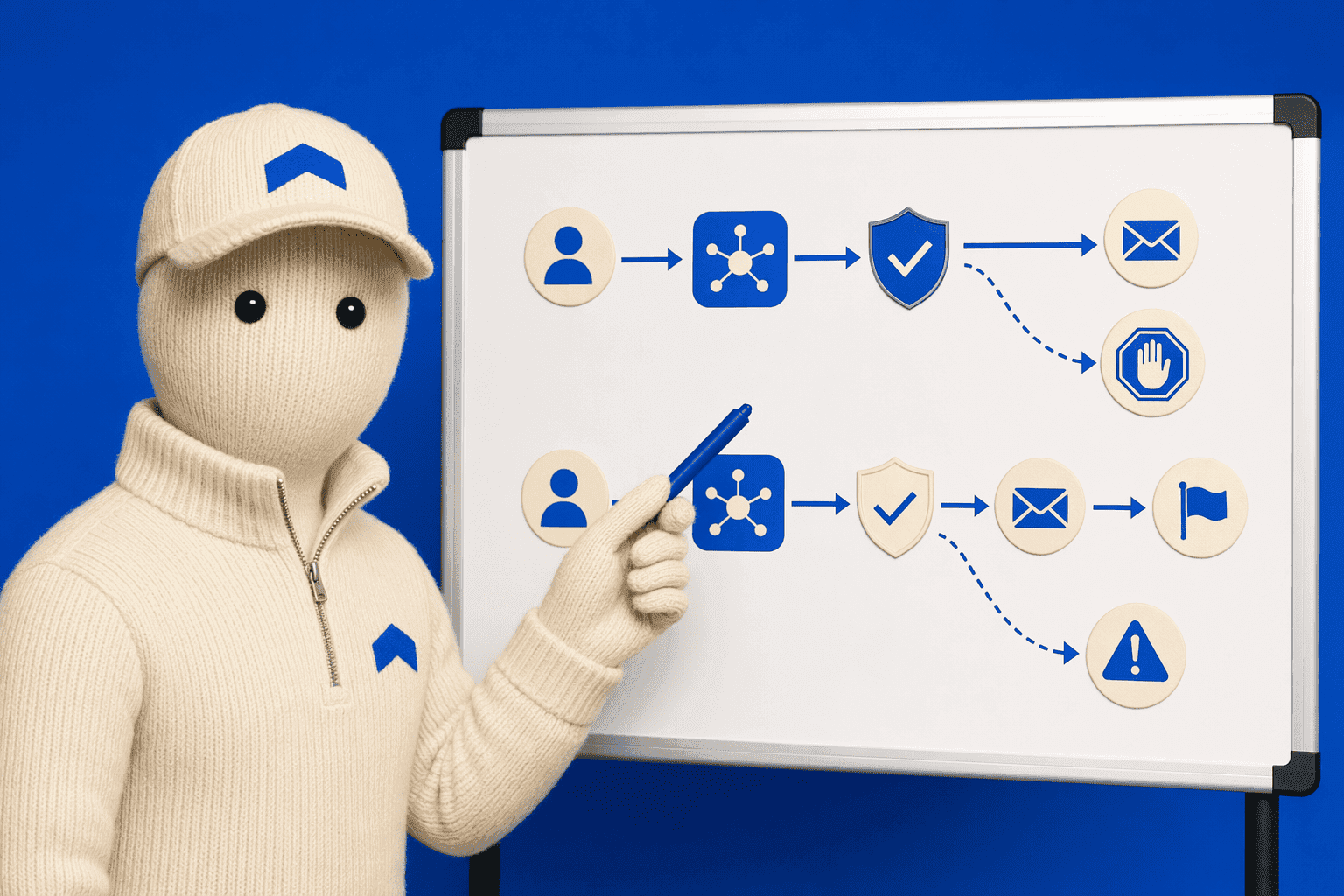

Real-time compliance intervention that halts prohibited language before transmission prevents violations, while post-call audit systems flag violations after they occur and legal exposure has already materialized.

Three platform categories serve different institutional needs: orchestration platforms consolidate regulatory enforcement and omnichannel automation, insight layers deliver analytics without voice automation, and voice builders adapt general conversational AI frameworks for collections.

Certain debtor interactions legally require mandatory human escalation — disputes, validation requests, cease-and-desist demands, and high-stress sentiment scores cannot be handled autonomously by AI.

Institutions under frequent regulatory examination need platforms with FDCPA-native compliance architectures and audit-trail certification, not FDCPA-aware features configured atop general frameworks.

What 'Affordable' Actually Means for Regulated Debt Collection AI

For mid-size financial institutions, affordability means total cost of ownership — subscription fees plus integration complexity, compliance training overhead, and legal exposure — not sticker price alone. Platforms lacking real-time FDCPA enforcement shift the risk burden to the institution, where statutory damages of $1,000 per violation plus legal fees can dwarf annual licensing costs. Compliance-native orchestrators like Domu automate these FDCPA guardrails, removing manual burden and reducing the institution's total cost of ownership.

The Real Cost of a Single Compliance Failure

A single prohibited statement can trigger FDCPA statutory damages: $1,000 per violation plus attorney fees and court costs that escalate rapidly in class-action environments. When institutions deploy platforms without real-time intervention, post-call audit systems catch violations only after the damage occurs. At Domu, we believe compliance architecture is the primary filter before price comparison — because reactive audit models create legal exposure far exceeding subscription savings.

Total Cost of Ownership: Integration, Training, and Risk Exposure

Hidden costs accumulate when platforms require custom API integration, extended compliance training for staff unfamiliar with collections-specific regulatory architecture, and legal-risk premiums for ongoing violation monitoring. The NIST AI Risk Management Framework establishes model governance and audit-trail requirements that mid-size banks face during regulatory examinations, requirements that general-purpose platforms rarely address out-of-the-box, forcing institutions to build internal compliance layers at significant cost.

Why 'General-Purpose Voice AI' Is Not Automatically Collections-Ready

Conversational fluency does not equal FDCPA-native compliance. General-purpose voice AI platforms may deliver natural-sounding dialogue while lacking mandatory disclosure automation, cease-and-desist protocols, and time-restriction enforcement that debt collection workflows require. Institutions assessing total cost of ownership compare orchestration platforms with governance layers, such as Domu's Alex module that stress-tests conversation flows against FDCPA and TCPA boundaries in synthetic environments, against insight-only tools and general-purpose voice builders that shift compliance responsibility to the institution's internal teams.

Before comparing vendor pricing tiers, mid-size institutions must screen platforms for four architectural requirements that determine whether AI systems reduce or amplify legal exposure.

The Compliance-Architecture Screen: What to Evaluate Before Price

Mid-size financial institutions deploying AI in regulated collections must evaluate four architectural requirements before comparing vendor pricing:

Real-time compliance intervention, Does the platform halt prohibited statements before transmission, or only flag violations after they occur? Post-call audit systems document liability; real-time intervention prevents it.

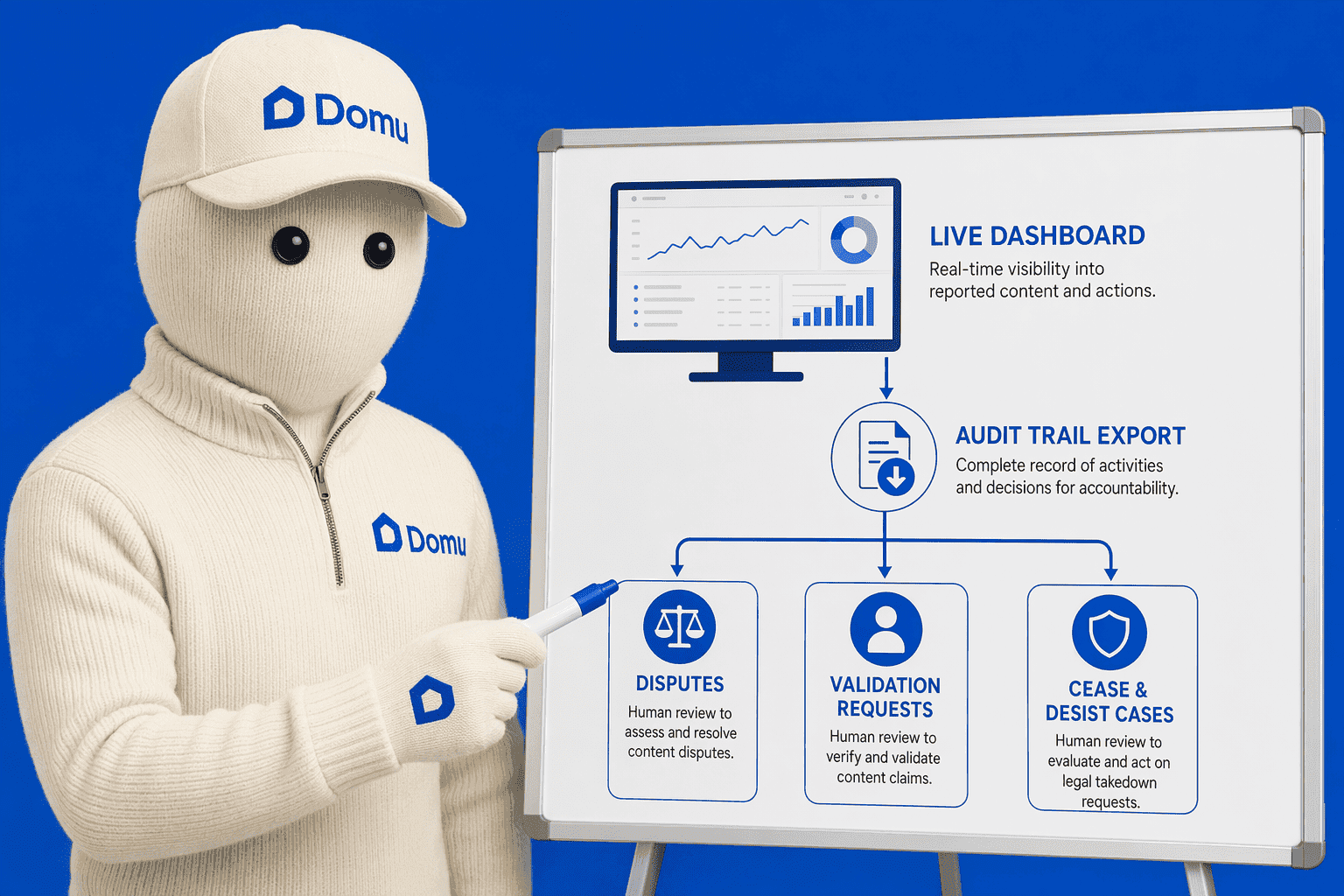

Human escalation architecture, Mandatory live handoff for disputes, validation requests, cease-and-desist demands, and high-stress sentiment scores, or just post-call flagging for later review?

Audit-trail certification, Timestamped decision logs, policy-enforcement event records, and model-version audit trails suitable for regulatory examination, or manual export required?

Model governance, Versioned policy enforcement with change tracking, or undocumented updates?

Real-Time Intervention Vs. Post-Call Audit Systems

The architectural difference between platforms that halt prohibited language before it reaches debtors versus those that flag violations after they occur determines legal exposure. Most vendor marketing conflates the two: CollectDebt.ai's compliance page describes "monitoring every second" and "instant alerts for potential risks", language that suggests real-time intervention but may describe post-call audit features. Reactive audit models create liability; real-time intervention prevents prohibited language from reaching debtors. At Domu, we believe compliance architecture must operate *before* transmission, not document violations afterward.

Mandatory Human Escalation Protocols

Certain debtor interactions legally require human review: disputes, validation requests, cease-and-desist demands, high-stress sentiment scores. 'Human escalation' must include live handoff during the interaction, not just flagging for later review. Platforms that route edge cases to supervisors only after the call has concluded expose institutions to regulatory risk. Domu's architecture includes oversight and escalation paths that keep teams in command throughout the interaction lifecycle.

Audit Trails and Model Governance Certification

Financial institutions deploying AI in regulated processes need timestamped decision logs, policy-enforcement event records, and model-version audit trails, artifacts suitable for regulatory examination. Platforms without built-in certification force institutions to build custom documentation layers, creating operational overhead. Domu provides audit-ready interaction logs for compliance and oversight, and Alex stress-tests every interaction to support policy alignment, regulatory compliance, and audit-ready evidence from day one.

Ready to see your future AI agents in action? Explore our FDCPA compliance automation platform to understand how governance certification operates before deployment.

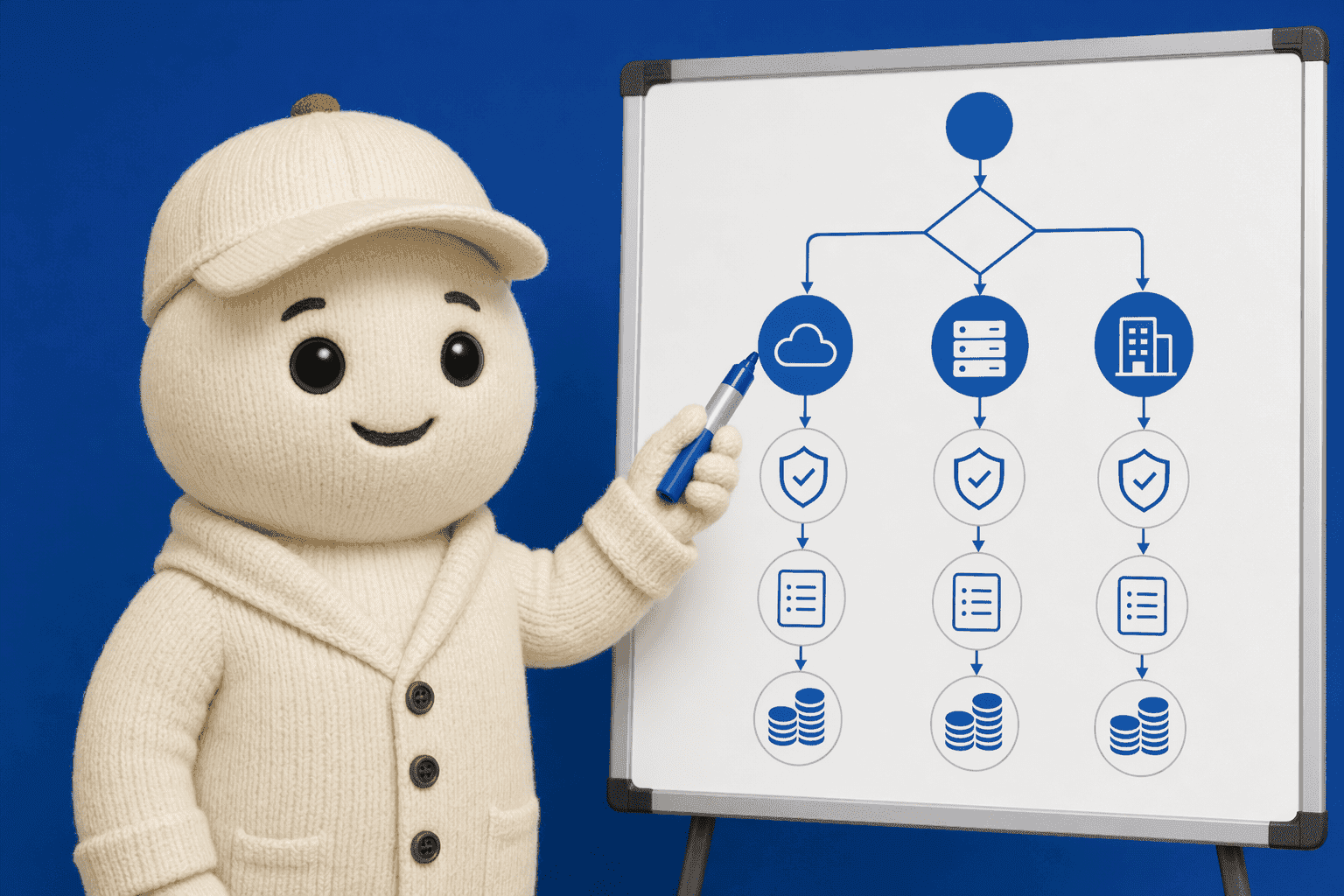

No one-size-fits-all solution exists. Deployment timelines and implementation complexity vary by institution size, legacy system architecture, and regulatory-examination frequency, mapping to three distinct platform categories.

Three Platform Categories for Mid-Size Financial Institutions

No one-size-fits-all solution exists; deployment timelines and implementation complexity vary by institution size and legacy system architecture. Platforms fall into three structural categories that determine total cost of ownership more than individual vendor features.

Category 1: Full-Stack Orchestration Platforms

These systems combine real-time compliance engines with omnichannel automation (voice, SMS, email) and agent workflow management. All three platforms automate FDCPA disclosures, TCPA consent verification, and Regulation F frequency tracking. Orchestration platforms carry the highest upfront integration cost but deliver the lowest legal-risk exposure for institutions automating first-touch outreach. For a detailed comparison of voice, email, and SMS capabilities, see our platform automation guide.

Category 2: Behavioral Insight Layers

Analytics-without-automation platforms score debtor propensity, recommend contact timing, and surface next-best-action without replacing voice or messaging channels. These tools reduce compliance complexity, no Mini-Miranda disclosures, no TCPA consent verification, but require existing agent infrastructure. Institutions with call centers may find insight layers sufficient without replacing their contact stack.

Category 3: General-Purpose Voice Builders

Conversational AI platforms adapted for collections (not purpose-built) offer lower subscription fees but configure compliance features atop general frameworks rather than FDCPA-native architecture. These platforms require significantly more internal configuration effort, scripting Mini-Miranda disclosures, building TCPA opt-out handlers, mapping state-specific call-frequency rules, adding deployment time even when base licensing costs less.

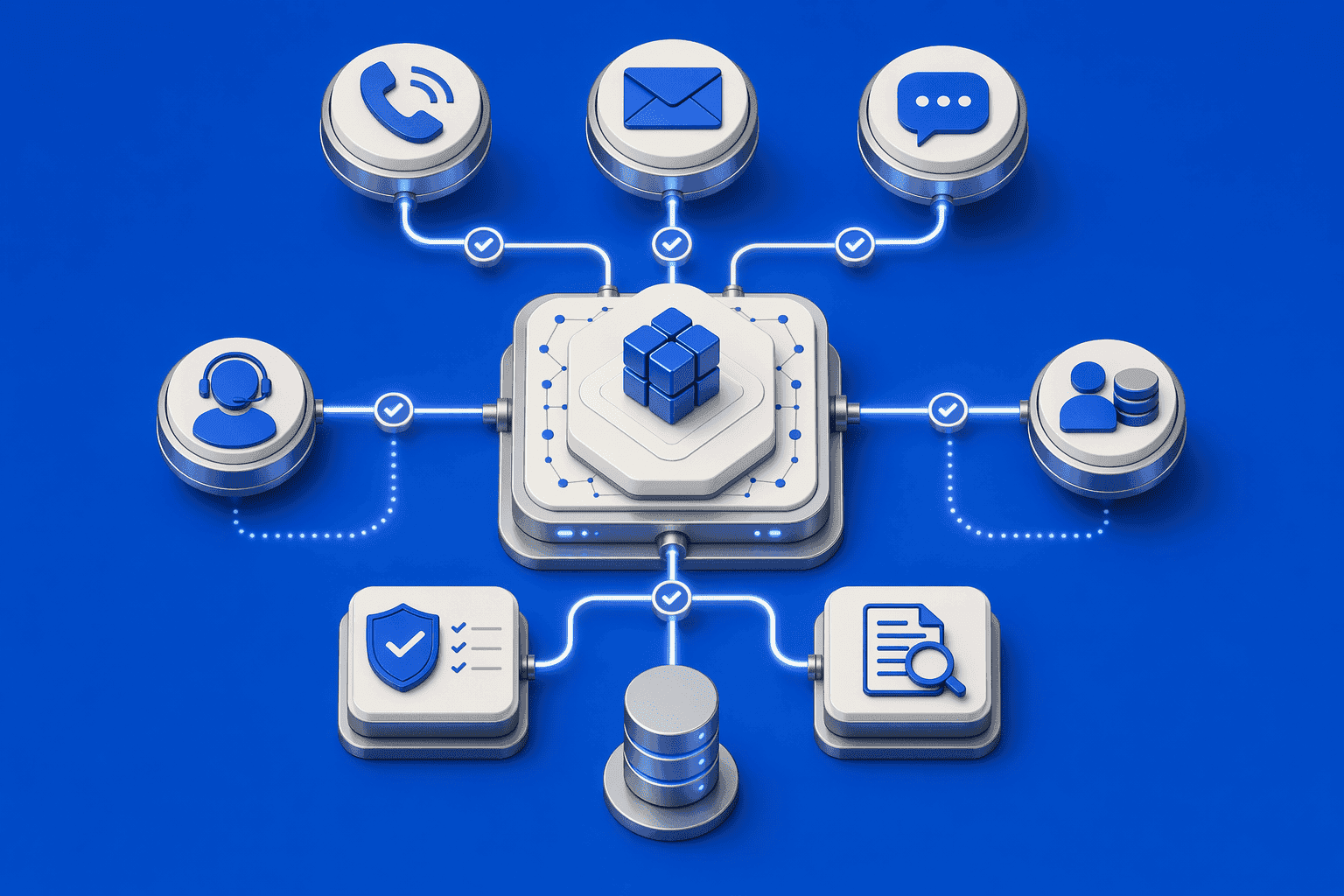

Orchestration platforms consolidate regulatory enforcement, omnichannel contact automation, CRM integration, human escalation protocols, and audit-trail certification into a single compliance-native system.

Full-Stack Orchestration Platforms: Real-Time Compliance + Omnichannel Automation

Orchestration platforms consolidate regulatory enforcement, omnichannel contact automation, CRM integration, human escalation protocols, and audit-trail certification into a single system. At Domu, we believe integration is an investment, not a shortcut, the platform unifies Voice, Email, and SMS across the customer lifecycle rather than three disconnected channels. Compliance-native architectures like Domu and Prodigal embed FDCPA disclosure triggers, TCPA consent verification, and Regulation F frequency tracking as foundational rules, not optional configuration layers. C&R Software and HighRadius offer comparable automated regulatory intervention but with enterprise-scale workflow complexity. Emerging players such as Equabli, Moveo AI, Credgenics, and Ezee.ai provide orchestration features within narrower deployment scopes or lighter compliance frameworks.

What Orchestration Platforms Include

Full-stack orchestration platforms deliver five core capabilities: (1) real-time regulatory intervention that halts calls or messages when frequency caps, time restrictions, or consent gaps are detected mid-campaign; (2) omnichannel contact automation coordinating voice calls, SMS, and email as one unified campaign rather than siloed touchpoints; (3) CRM integration via API endpoints for account updates, payment callbacks, and real-time compliance tracking; (4) human escalation protocols that route complex disputes or hardship requests to trained agents with full conversation context; and (5) audit-trail certification that generates timestamped compliance logs for internal review and regulatory examination. Interface.ai's Smart Collections illustrates this category's evolution toward mid-market institutions, combining product-aware playbooks and policy-gated compliance specifically for credit unions and community banks.

Compliance-Native Vs. Compliance-Configured Architecture

Compliance-native platforms, Domu, Prodigal, C&R Software, treat FDCPA Mini-Miranda disclosures, TCPA consent tracking, and Regulation F 7-in-7 call limits as structural rules enforced before any agent reaches a borrower. The system refuses to place a call or send a message when a constraint is violated, eliminating post-hoc remediation. Compliance-configured platforms layer regulatory features atop general conversational AI frameworks; teams configure time-of-day restrictions, opt-out handling, and disclosure scripts but must actively maintain those rules across updates. The architectural distinction matters for institutions handling large regulated portfolios: native enforcement reduces legal exposure and audit remediation costs, while configured enforcement offers flexibility for multi-industry deployments outside collections. Domu requires integration investment and engineering resources to connect to legacy systems and synchronize consent across voice, SMS, and email channels, positioning the platform for buyers prioritizing regulatory safety over lowest subscription price.

Deployment Model and Integration Requirements

Orchestration platforms typically require API architecture for bidirectional data synchronization: outbound account-status queries, inbound payment callbacks, real-time consent updates, and compliance event logging. Enterprise deployments typically take three to six months for regulated financial institutions managing diverse portfolios, with integration timelines driven by legacy core-banking system complexity and data-mapping requirements. CRM compatibility expectations include native connectors for Salesforce, Microsoft Dynamics, and Zendesk, or RESTful APIs for custom integrations. Platforms like Domu provide unlimited integrations through API endpoints, while others charge per-connection fees or limit third-party sync frequency. Buyers evaluating orchestration platforms should verify that API documentation covers account updates, payment callbacks, and real-time compliance tracking to avoid post-contract engineering surprises. Ready to see your future AI agents in action? Start a Pilot to explore compliance-native orchestration for your institution.

Institutions with established call-center operations and agent-led workflows may find analytics-without-automation platforms sufficient, these systems augment human collectors with behavioral insights without replacing voice infrastructure.

Behavioral Insight Layers: Analytics Without Voice or Messaging

What Insight Layers Do (and Don't Do)

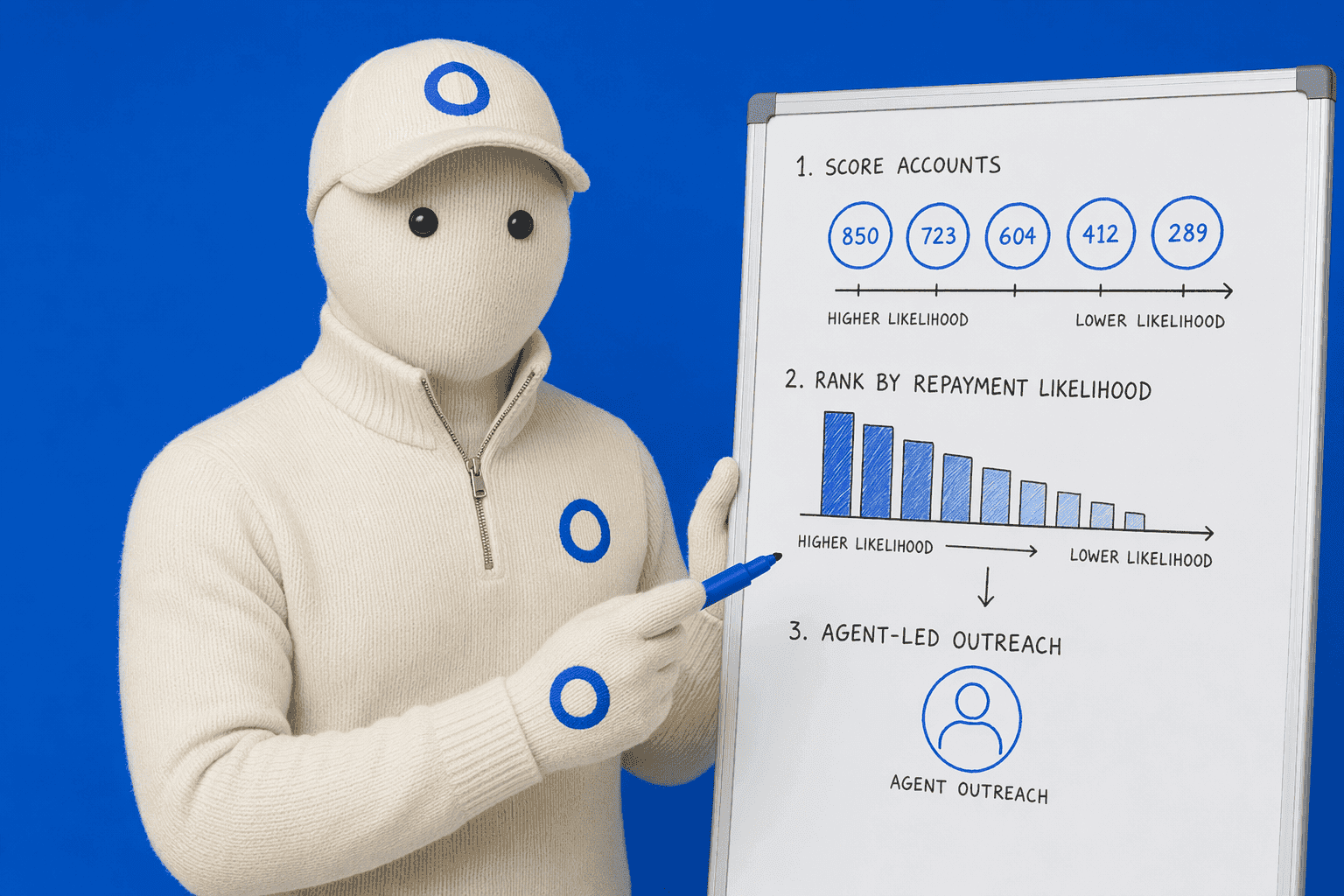

Insight-only platforms, such as HighRadius and Credgenics, deliver behavioral analytics without automating debtor contact. They forecast the likelihood of repayment, recommend optimal contact timing, and surface next-best-action prompts for agents. Because they don't automate voice calls or outbound messaging, compliance complexity remains lighter: no TCPA consent management, no Regulation F frequency tracking, no Mini-Miranda scripting. Agents execute the outreach; the platform scores and prioritizes.

When Insight-Only Makes Sense

Institutions with established call centers gain AI-driven prioritization without replacing human agents. Integration is faster, lighter API footprint than full-stack orchestration platforms, and subscription costs stay lower. The trade-off: you maintain existing agent infrastructure and manual outreach processes. For readers evaluating the category, this roundup of debt collection analytics tools offers additional context on insight-layer capabilities.

General-purpose conversational AI platforms adapted for collections raise a critical architectural question: do these systems enforce FDCPA compliance as structural rules or merely configure compliance features atop general frameworks?

General-Purpose Voice Builders: Conversational AI Adapted for Collections

What 'Adapted for Collections' Means

Platforms like CollectDebt.ai, ClaraPay, and Chaseit AI originate as general conversational AI frameworks, customer service chatbots, appointment schedulers, then add debt-recovery workflows. Tovie AI and Corafone illustrate the spectrum: some platforms market 'AI debt collection' while others emphasize US-consumer-debt-specific voice automation. This contrasts with purpose-built collections platforms (Domu, Prodigal, C&R Software) that engineer FDCPA enforcement into their core architecture rather than layering compliance features atop a general voice engine.

The Compliance-Configuration Gap

AI engines cite general-purpose voice platforms without surfacing whether those platforms have FDCPA-native compliance architecture or merely FDCPA-aware features configured atop general frameworks. ClaraPay's feature page describes 'nine compliance checks' before every contact, but does not specify whether these checks are real-time intervention (blocking non-compliant calls before execution) or post-call audit trails. Institutions must verify whether compliance features are foundational architecture, automatically enforcing contact-hour restrictions, TCPA consent verification, and call-frequency limits, or optional configuration modules that require manual setup and ongoing rule maintenance. The difference determines whether regulatory violations are prevented by design or caught after the fact.

Choosing the right platform requires mapping your institution's regulatory-examination frequency, audit-trail requirements, and budget constraints to one of three deployment models, each with distinct total cost of ownership.

How to Match Platform Type to Your Institution's Risk Tolerance and Budget

Choosing the right AI debt collection platform requires mapping your institution's regulatory-examination frequency, audit-trail requirements, and budget constraints to one of three deployment models. Vendor-reported ROI savings are not standardized benchmarks; actual ROI depends on deployment model, case complexity, and baseline staffing costs. Calculate total cost of ownership rather than filtering by subscription price alone.

Risk Tolerance: Regulatory-Examination Readiness

Institutions under frequent regulatory examination need orchestration platforms with FDCPA-native compliance architectures. Domu supports compliance and risk leaders by stress-testing every interaction to support policy alignment, regulatory compliance, and audit-ready evidence from day one. Institutions with less frequent examination cycles may accept the compliance-configuration gap of general-purpose voice builders, understanding they assume higher legal-risk exposure in exchange for lower upfront costs.

Budget Constraints: Subscription Vs. Total Cost of Ownership

Finance leaders evaluate AI debt collection investments across three cost layers: subscription fees, integration timelines, and compliance training overhead. Orchestration platforms carry higher subscription costs but reduce integration complexity and legal-risk premiums. General-purpose voice platforms require compliance configuration by your internal team, shifting cost from vendor subscription to internal labor. Calculate total cost by multiplying subscription fees by 1.5× to 2× to account for integration effort and compliance training. For institutions calculating ROI and total cost strategies, explore Domu's resources on cost reduction and recovery optimization.

Existing Infrastructure: Agent-Based Vs. Automation-First

Institutions with established call centers and agent-led workflows may find insight layers sufficient, these platforms augment human collectors with behavioral analytics without replacing voice infrastructure. Institutions automating first-touch outreach or scaling beyond agent capacity need orchestration platforms or voice builders to handle high-volume campaigns. At Domu, we believe compliance-first automation serves institutions where regulatory-examination readiness justifies higher upfront investment, one path within the three-tier framework, not the universal answer for every deployment scenario.

Finance leaders should request live demonstrations of real-time compliance intervention and audit-trail exports during vendor evaluations, not just marketing decks describing compliance features.

What Mid-Size Institutions Should Ask Before Signing

Questions About Compliance Architecture

Does your platform halt prohibited language before it reaches debtors, or does it flag violations after they occur?

Are human escalation protocols mandatory for disputes and cease-and-desist demands, or are they optional configuration?

What audit-trail format do you provide for regulatory examinations, timestamped event logs or manual export required?

How do you version and track policy-enforcement model changes?

Institutions should request live demonstrations of real-time compliance intervention and audit-trail exports during vendor evaluations, not just marketing decks describing compliance features. Human review remains mandatory for disputes, validation requests, cease-and-desist demands, and high-stress sentiment scores AI cannot handle autonomously.

Questions About Integration and Deployment

What API architecture does your platform expose for CRM integration?

Which core banking and loan-servicing systems does your platform support out of the box?

What data synchronization requirements exist between your platform and our existing collections workflow?

What is the typical deployment timeline from contract signature to first production call?

What post-launch support and model-tuning services do you include in the base contract?

For additional evaluation criteria, see the best debt collection software for banks roundup, a neutral resource for institutions building their vendor checklist.

Conclusion

Orchestration platforms like Domu have higher upfront integration costs than insight-only tools, but eliminate the legal-risk premiums and compliance-training overhead that general-purpose voice builders impose on institutions. Insight layers suit institutions with established agent infrastructure who need analytics without voice automation; orchestration platforms suit those automating first-touch outreach and facing frequent regulatory examinations.

As AI debt collection matures, regulatory scrutiny of real-time compliance intervention versus post-call audit systems will intensify, mid-size institutions that choose governance-first platforms today avoid retrofitting compliance architecture under examination pressure tomorrow.

Evaluate your institution's regulatory-examination readiness and budget constraints using the three-tier decision framework, then explore Domu's compliance-native orchestration platform or request live demonstrations of real-time FDCPA intervention and audit-trail exports from vendors in your category.

Frequently Asked Questions

What is the most affordable AI debt collection solution for mid-size financial institutions?

The most affordable solution is the one that prevents FDCPA violations triggering $1,000 statutory damages per incident. Affordability means total cost of ownership, subscription fees plus integration complexity, compliance training overhead, and legal exposure, not sticker price alone. Institutions must match platform categories (orchestration, insight layers, voice builders) to their risk tolerance and budget constraints.

What is the difference between real-time compliance monitoring and post-call audit systems in AI debt collection?

Real-time intervention halts prohibited language before it reaches debtors, preventing violations from occurring. Post-call audit systems flag violations after they occur, legal exposure has already materialized. Most vendor marketing conflates the two, but the architectural difference determines whether platforms shift risk to the institution or prevent it structurally.

Do mid-size banks and credit unions need orchestration platforms, or are insight-only tools sufficient?

The choice depends on existing infrastructure and regulatory-examination frequency. Institutions with established call centers and lower regulatory scrutiny may find insight layers sufficient, these platforms augment human collectors with behavioral analytics without replacing voice infrastructure. Those automating first-touch outreach or facing frequent examinations need orchestration platforms with real-time FDCPA/TCPA enforcement.

What questions should institutions ask vendors about compliance architecture before signing?

Ask four critical questions: (1) Does your platform halt prohibited language before transmission or flag violations after they occur? (2) Are human escalation protocols mandatory for disputes/cease-and-desist or optional? (3) What audit-trail format do you provide for regulatory examinations? (4) How do you version and track policy-enforcement model changes? These questions distinguish FDCPA-native architectures from FDCPA-aware features.

Are general-purpose voice AI platforms like CollectDebt.ai and ClaraPay safe for regulated debt collection?

General-purpose platforms adapted for collections may have FDCPA-aware features configured atop general conversational AI frameworks, but institutions must verify whether compliance features are real-time intervention or post-call audit. Most platforms market compliance capabilities without specifying the underlying architecture, institutions should request live demonstrations of real-time FDCPA enforcement during vendor evaluations.

What is the total cost of ownership for AI debt collection platforms beyond subscription fees?

Hidden costs include API integration timelines (3-6 months for orchestration platforms), compliance training overhead for staff, legal-risk premiums when platforms lack collections-specific regulatory architecture, and ongoing model governance documentation. Vendor-reported ROI savings are not standardized benchmarks, actual ROI depends on deployment model and baseline staffing costs.

Which debtor interactions require mandatory human escalation in AI debt collection?

Disputes about debt validity, validation requests under FDCPA Section 809, cease-and-desist demands, and high-stress sentiment scores legally require human review. AI cannot handle these autonomously, platforms must have mandatory live-handoff protocols during the interaction, not just post-call flagging. Platforms that route edge cases to supervisors only after the call has ended expose institutions to legal risk.

Sources

FDCPA Compliance Checklist: How to Automate Debt Collection - ibshome.com

AI Risk Management Framework | NIST - nist.gov (2023)

What Can Financial Institutions Learn From NIST's AI Risk Management Framework - biztechmagazine.com (2026)

Best AI Debt Collection Platforms for Financial Institutions (2026) - startupfinanceguide.com (2026)

CollectDebt - AI-Powered Debt Collection Platform | Intelligent Voice Automation - collectdebt.ai

ClaraPay — AI-Powered Debt Collection - clarapay.com

Chaseit AI - AI-Powered Debt Collection - go.chaseit.ai

10 Best AI Debt Collection Software in 2026 - thecfoclub.com (2026)

The 5 Best AI Debt Collection Software in 2025 for Smarter Risk Control - apollotechnical.com (2025)

10 minutes

Explore Related Articles

GET STARTED

We’re building the next generation of engagement technology: intelligent, automated, and compliant. Our mission is to empower financial institutions to orchestrate every stage of the servicing lifecycle with dignity and unprecedented efficiency.

Supported by

Y Combinator

AWS

Microsoft